NFRS 9 – ECL Guidelines – Nepal Rastra Bank

The updated NFRS 9: Financial Instruments standard was initially set to be effective from July 16, 2021. However, challenges like the COVID-19 pandemic, limited time, and lack of technical expertise led to its full implementation being postponed to the fiscal year 2080/81 for banks and financial institutions. Therefore, the provisions of NFRS 9, including expected credit loss, will be fully effective from FY 2081/82.

The board of directors and senior management of licensed banks and financial institutions are responsible for preparing and presenting financial statements according to Nepal Financial Reporting Standards. To ensure consistent and prudent application of NFRS 9 in the banking sector, Nepal Rastra Bank has drafted guidelines for implementing the expected credit loss provision of NFRS 9. These guidelines are based on international best practices and regulatory guidelines from various jurisdictions.

Objectives of Guidelines

The guidelines aim to provide supervisory guidance for implementing ECL, promote uniformity and comparability among banks, set out criteria for determining significant increases in credit risk, prescribe a regulatory backstop for impairment determined under the ECL model, and strengthen the accounting recognition of loan loss provisions.

Scope of Expected Credit Loss

Licensed banks and financial institutions must calculate expected credit losses for various financial assets, including those measured at amortized cost and fair value through other comprehensive income, lease receivables, contract assets, loan commitments, and financial guarantee contracts.

Basic Core Principles regarding ECL accounting framework

Banks and financial institutions should adopt methodologies that are proportional to their size and complexity, consider a wide range of reasonable and supportable information, and include forward-looking information. Changes in credit risk should be reflected symmetrically in the measurement of loss allowances.

Principles for Sound Credit Risk Management and for ECL

Banks must ensure they have effective credit risk practices and internal controls for determining adequate allowances. They should adopt sound methodologies for assessing and measuring credit risk and have policies and procedures for validating models used in this process. The use of experienced credit judgment is crucial, especially in considering forward-looking information.

Requirement of Approved ECL policies

Banks must have written policies regarding ECL, approved by their board of directors. These policies should cover roles and responsibilities, control procedures for developing and validating ECL models, criteria for assessing loan portfolios, and sources for forward-looking information.

Expected Credit Losses

Expected Credit Losses are probability-weighted estimates of credit losses over the life of a financial instrument. Banks must recognize 12-month expected credit losses for financial instruments with low credit risk or no significant change in credit risk since initial recognition. Lifetime expected credit losses must be recognized for financial instruments with a significant increase in credit risk since initial recognition.

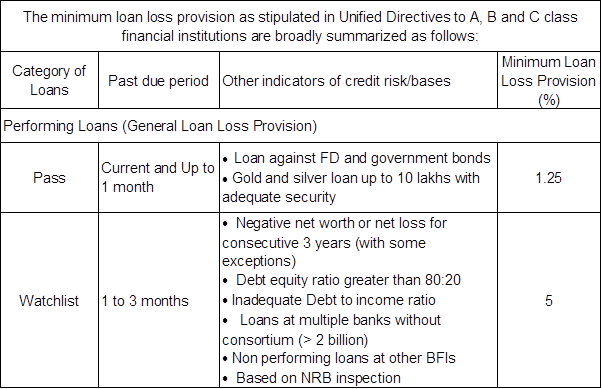

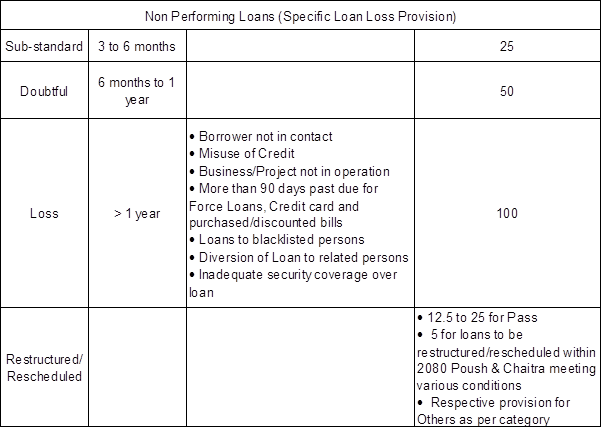

Indicators of significant increase in credit risk

Various conditions indicate a significant increase in credit risk, such as being more than 30 days past due, a significant increase in the Probability of Default, downgrading of risk ratings, and deterioration in the creditworthiness of borrowers.

Interest income recognition

Interest income on financial assets should be calculated based on their classification in different stages of credit risk.

{kind=link}