Functional Currency – Ind AS 21

Executive summary of Functional Currency

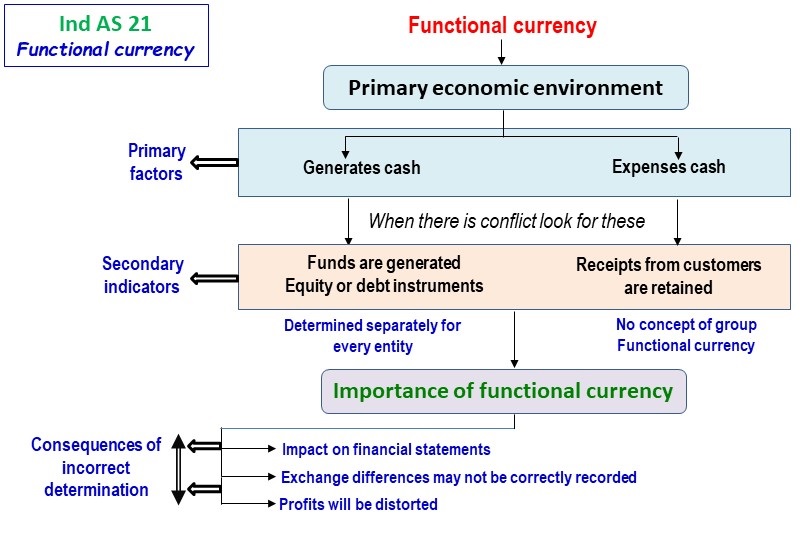

Functional currency is determined based on the primary economic environment in which it operates.

The primary economic environment is determined based on two primary factors as specified in the Standard viz., the currency in which cash is generated and the currency in which major expenses are incurred by the entity.

When there is a conflict between the two primary factors, then the entity should look for further indicators viz., the currency in which funds are generated which could be either equity or debt instruments and the currency in which the receipts from the customers are retained.

These two are known as the secondary indicators. The entity need to look for secondary indicators only when there is conflict in the primary factors.

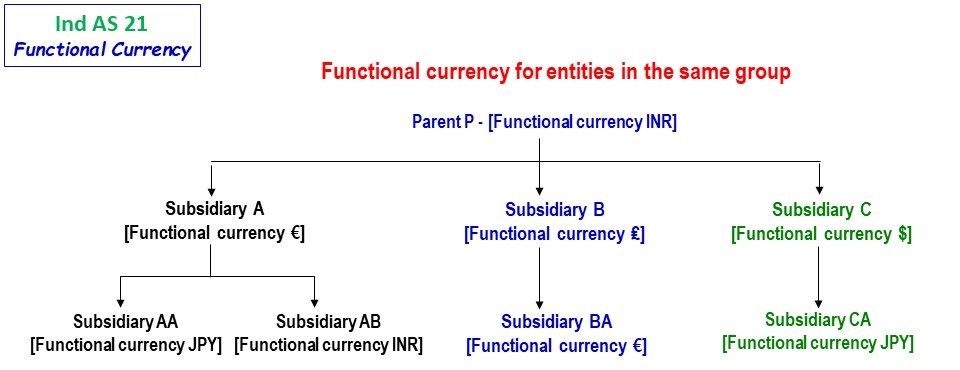

It should be noted that the functional currency is determined separately for every entity, as there is no concept of group functional currency.

The importance of functional currency cannot be over-emphasized, as it has a serious impact on the financial statements.

Exchange differences may not be correctly recorded if the functional currency is not determined properly.

Profits may also be completely distorted.

These are the consequences of incorrect determination of functional currency.

What is functional currency?

- The functional currency of an entity is the currency of the primary economic environment in which that entity operates

- The primary economic environment in which an entity operates is normally the one in which it primarily generates and expends cash

- The functional currency is determined separately for individual entities

- There is no such thing as a “group functional currency”

- Ind AS 21 gives the factors, primary and additional, that to determine the functional currency of an entity

Determination of functional currency

- As a first step, the factors that are specified in Ind AS 21 should be applied. The functional currency cannot be chosen freely by an entity, as this has to comply with the factors mentioned in the standard

- Also once the functional currency is determined, it cannot be changed unless there is a change in the underlying circumstances

Primary indicators

- The currency that mainly influences the sale price for its goods and services is the functional currency of the entity

- For example, if the sale prices are denominated in INR, then INR is the functional currency of the entity

- Functional currency is the currency of the country whose competitive forces and regulations mainly influence the pricing policy

- The functional currency is also determined based on the currency and other costs of providing goods or services

Priority is given to primary indicators

- If there is a conflict, based on the facts and circumstances, to determine the functional currency, then certain secondary indicators should be considered

- The secondary indicators are designed to provide additional supporting evidence to determine an entity’s functional currency

Secondary indicators

- Functional currency is the currency in which the funds are generated, which could be funds raised through debt instruments and/or equity instruments

- Functional currency is the currency in which receipts from customers are retained by an entity

Importance of functional currency

- If a functional currency is determined incorrectly, it will have a major impact on the financial statements

- Transactions, which are in effect foreign currency transactions, will be recorded as if they were the functional currency of the entity or vice-versa. Exchange differences on translation will be recognised on transactions for which there will be no foreign exchange difference

- Similarly, transactions that should have caused foreign exchange differences to be recognised will not be provided for having a significant impact on both the profit and loss account and balance sheet

Foreign operations – Ind AS 21

Exchange differences on monetary items

Exchange differences from non-monetary items

Difference between monetary and non-monetary items

Treatment of exchange differences – Ind AS 21

Presentation Currency – Ind AS 21

Objectives, Scope & Benefits Ind AS 21

Exchange differences from the presentation currency

Miscellaneous items – Ind AS 21

Transaction are covered by Ind AS 21

Recognition and measurement – Ind AS 21

Transaction are outside the scope of Ind AS 21

Financial statements presented in any currency

Difference between FX translation and FX revaluation

{kind=link}