Presentation Currency – Ind AS 21

Executive summary of Presentation currency

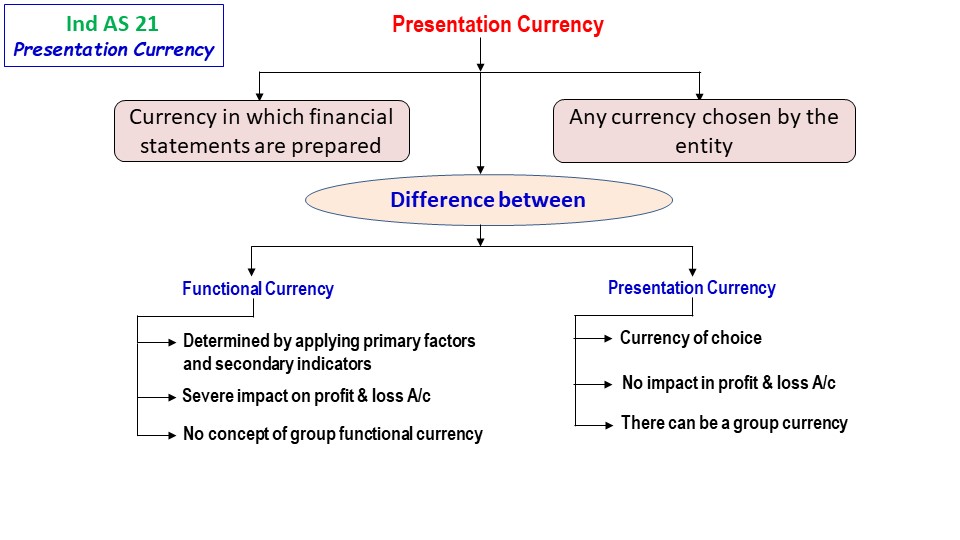

Let us understand what is a presentation currency and how it is different from the functional currency.

Presentation currency is the currency in which the financial statements are prepared.

This can be in a currency chosen by the entity as the entity is free to choose its own currency.

This is mainly for the purpose of presenting the financial statements to the stake holders who are located in another geographical area having a different local currency.

The main difference between a functional currency and the presentation currency should be understood very clearly.

Functional currency is determined by applying the factors that are specified in the standard which are known as primary factors.

If there is a conflict in the primary factors, then the entity should look for secondary indicators.

Selecting the correct functional currency is extremely important as this will have a severe impact on the profit and loss account if not selected properly.

The functional currency is determined individually for different entities even within the same group and there is no such concept called group functional currency.

However, presentation currency is selected by the entity as a matter of choice.

Selecting any currency will have no impact on the profit and loss account. There could also be a group presentation currency if the group so decides.

What is presentation currency?

- Presentation currency is the currency in which the financial statements are presented

- The presentation currency can be any currency chosen by the entity to present its financial statements to the investors or prospective investors or the other stake holders

Difference between functional currency and presentation currency

- Functional currency is determined based on applying certain indicators specified in the standard viz., primary indicators and secondary indicators

- Priority is given to the primary indicators before considering the secondary indicators which are mainly designed to provide additional supporting evidence for determining the functional currency

- Presentation currency is a currency chosen by the entity to present its financial statements. An entity has a flexible choice to select any currency

Impact on profit and loss

- Determining proper functional currency is essential as it has a major impact on the net profit of the entity

- Incorrect determination of functional currency leads to inaccurate computation of profit and loss account

- However, selected currency has no impact on the net profit in the case of presentation currency

Exchange differences

- Exchange differences on account of presenting the financial statements in a currency other than the functional currency are recognised in other comprehensive income

- The exchange differences do not impact the profit and loss account, as it is not recognised as either income or expense for the period concerned

- Also, a presentation currency does not impact the present and future cash flows of the entity

Monetary and non-monetary items

- A monetary item represents an asset or liability having a right to receive or an obligation to deliver a fixed or determinable number of units of a currency

- The essential feature is that a monetary item should be convertible into a number of determinable number of units of currency

- For example, if an entity borrows money in foreign currency, then the entity should report the same amount in foreign currency as per the terms of the borrowings, irrespective of the foreign exchange rate between the foreign currency in which the amount is borrowed and the functional currency of the entity

- Another example can be an investment made by an entity in a debt instrument, which is classified as measured at amortised cost in foreign currency

- Here, the entity expects to hold the debt instrument till the date of maturity and on such date the entity would get the investments back from the issuer to the extent of the same amount as the maturity value irrespective of the foreign exchange rate between the functional currency of the entity and the foreign currency in which the investment in debt instruments is made

Other Examples

- Pension and other employee benefits to be paid in cash

- Provisions that should be settled by an entity in cash

- Dividends that are payable by an entity which are recognized as liability

Non-monetary items

- In a non-monetary item, there is no existence of the right to receive or the obligation to pay a fixed or determinable number of units of a currency

Example

- An entity has invested in equity shares denominated in foreign currency. The investments would be realised by the entity whenever the same is liquidated and the money that would be realised would be converted into the functional currency, depending upon the foreign exchange rate

- In other words, the entity cannot insist on the return of the amount at a pre-determined number of units of such foreign currency

Other examples

- Prepaid expenses like amounts paid for goods and services

- Investments in intangible assets

- Investments in property, plant and machinery

- Amount of goodwill and inventories

Foreign operations – Ind AS 21

Exchange differences on monetary items

Exchange differences from non-monetary items

Difference between monetary and non-monetary items

Treatment of exchange differences – Ind AS 21

Objectives, Scope & Benefits Ind AS 21

Functional Currency – Ind AS 21

Exchange differences from the presentation currency

Miscellaneous items – Ind AS 21

Transaction are covered by Ind AS 21

Recognition and measurement – Ind AS 21

Transaction are outside the scope of Ind AS 21

Financial statements presented in any currency

Difference between FX translation and FX revaluation

{kind=link}