Norms on Restructuring of Advances by NBFCs

Non-Banking Financial Companies (NBFCs) play a crucial role in the financial system, especially in the restructuring of advances. The norms and guidelines that govern the restructuring of advances by NBFCs, including the Corporate Debt Restructuring (CDR) Mechanism and the Small and Medium Enterprises (SME) Debt Restructuring Mechanism.

Applicability and Framework

The prudential norms discussed here apply to all types of restructurings, including those under the CDR Mechanism. The framework for CDR Mechanism and SME Debt Restructuring Mechanism is detailed in the Master Circular on Prudential norms on Income Recognition, Asset Classification, and Provisioning pertaining to Advances.

Key Concepts and Definitions

The norms include definitions and concepts crucial for understanding and implementing the restructuring process. These are detailed in the appendices of the document.

Projects Under Implementation

For projects financed by NBFCs, it’s essential to clearly define and document the ‘Date of Completion’ and the ‘Date of Commencement of Commercial Operations’ (DCCO). This is crucial for the appraisal and sanctioning of loans. Projects often face delays due to reasons beyond the control of promoters, like legal issues or delays in government approvals. These factors can necessitate the restructuring or rescheduling of loans.

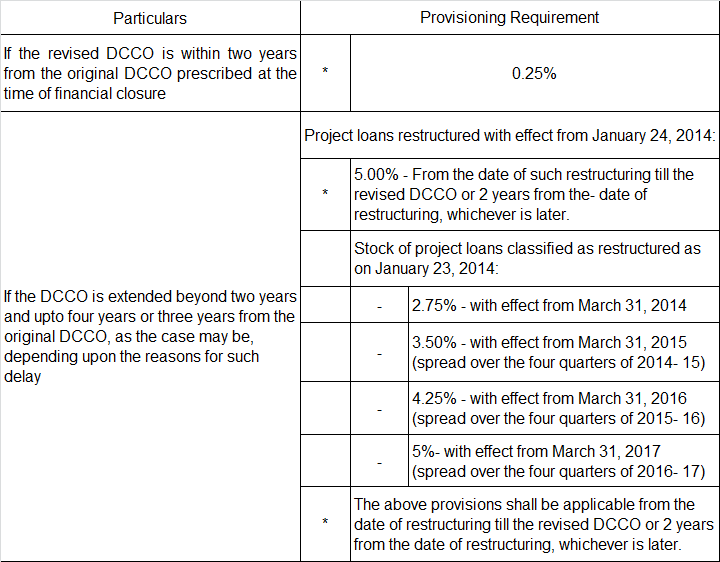

NBFCs shall maintain following provisions on such accounts as long as these are classified as standard assets in addition to provision for diminution in fair value:

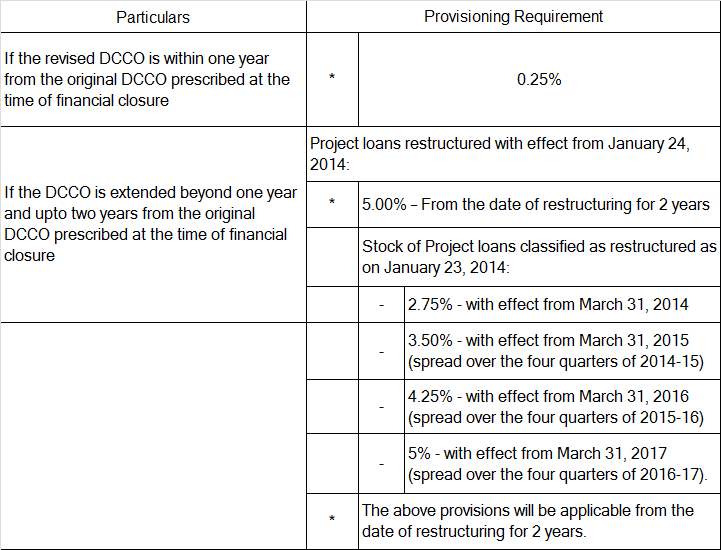

NBFCs shall maintain following provisions on such accounts as long as these are classified as standard assets apart from provision for diminution in fair value due to extension of DCCO:

Asset Classification Norms

The norms categorize project loans into infrastructure and non-infrastructure sectors, with specific guidelines for each. The classification of a loan as a Non-Performing Asset (NPA) and its subsequent treatment depends on various factors, including delays in project completion and restructuring.

Provisioning Requirements

NBFCs must adhere to specific provisioning requirements for restructured accounts. These requirements vary based on the extension of the DCCO and the reasons for such delays. The norms outline the provisioning percentages applicable under different scenarios.

Treatment of Standard Assets

The extension of DCCO within certain limits does not automatically categorize a loan as restructured, provided other terms and conditions remain unchanged. The norms specify the conditions under which a project loan can retain its standard asset classification even after restructuring.

Funding of Cost Overruns

NBFCs are allowed to fund cost overruns under specific conditions. This includes funding additional ‘Interest During Construction’ and other cost overruns within prescribed limits.

Change in Ownership

The norms also address scenarios where a change in ownership occurs. In such cases, NBFCs may extend the DCCO, subject to certain conditions, without changing the asset classification of the account.

Income Recognition

Income recognition for projects under implementation is based on their classification as ‘standard’ or ‘substandard’ assets. NBFCs must adhere to specific guidelines for income recognition and provisioning in these cases.

General Principles for Restructured Advances

The document outlines the eligibility criteria for restructuring, asset classification norms, income recognition, and provisioning norms for restructured advances. It emphasizes the need for financial viability and reasonable certainty of repayment as prerequisites for restructuring.

Disclosure Requirements

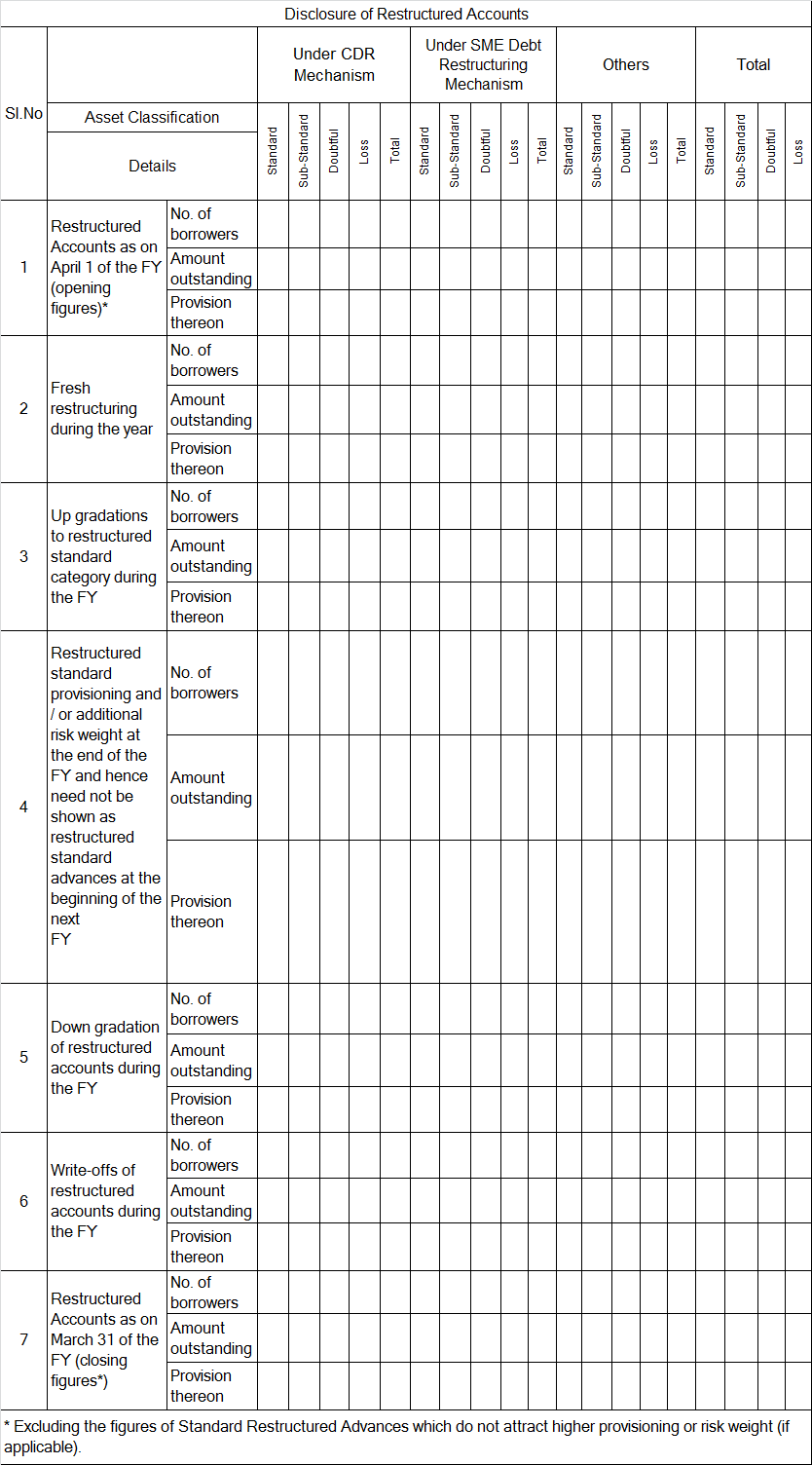

NBFCs are required to disclose detailed information about restructured accounts in their annual balance sheets. This includes the number and amount of advances restructured, the diminution in the fair value of restructured advances, and other relevant details.

CDR and SME Debt Restructuring Mechanisms

The document provides an overview of the CDR Mechanism and the SME Debt Restructuring Mechanism, outlining their objectives, scope, and operational guidelines. These mechanisms are designed to facilitate the timely and efficient restructuring of debts.

Introduction to RBI – NBFC Scale Based Regulation

Regulations applicable for NBFC-BL

Regulations applicable for NBFC-ML

Regulatory Instructions for NBFC-UL

Directions for NBFC – Micro Finance MFIs

Specific Directions for NBFC-Factors and NBFC-ICCs

Specific Directions for Infrastructure Debt Funds IDFs-NBFC

Scoring Methodology for Identification of NBFC as NBFC-UL

Regulatory Guidance on Implementation of Ind AS by NBFCsv

Early Recognition of Financial Distress

Flexible Structuring of Long Term Project Loans to Infrastructure and Core Industries

Guidelines on Liquidity Risk Management Framework

Disclosures in Financial Statements – Notes to Accounts of NBFCs

Managing Risks and Code of Conduct in Outsourcing of Financial Services by NBFCs

Guidelines for Credit Default Swaps – NBFCs as Users

Guidelines on Private Placement of NCDs by NBFCs

Guidelines for Entry of NBFCs into Insurance

Guidelines on Issue of Co-Branded Credit Cards

Guidelines on Distribution of Mutual Fund Products by NBFCs

Guidelines on Perpetual Debt Instruments

Guidelines on Liquidity Coverage Ratio (LCR)

Balance Sheet Disclosure Guidelines for NBFCs in Middle Layer and Above

Self-Regulatory Organization (SRO) for NBFC-MFIs – Criteria for Recognition

{kind=link}