Regulations applicable for NBFC-BL

Registration

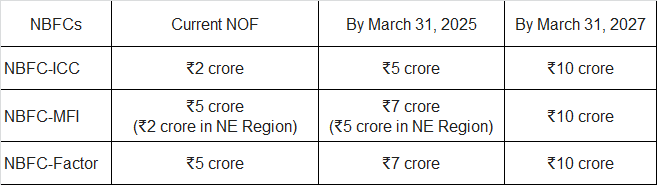

A non-banking financial institution (NBFC), specific financial requirements must be met. The Reserve Bank of India (RBI) has set these requirements. For NBFCs like NBFC-ICC, NBFC-MFI, and NBFC-Factor, the required Net Owned Fund (NOF) is ₹10 crore. However, for NBFC-P2P, NBFC-AA, and some others that don’t use public funds and have no customer interface, the NOF is ₹2 crore. For NBFC-IFC and IDF-NBFC, it’s ₹300 crore.

Existing NBFCs need to gradually increase their NOF to ₹10 crore. This increase is planned over a few years. For example, an NBFC-ICC currently at ₹2 crore must reach ₹5 crore by March 31, 2025, and ₹10 crore by March 31, 2027. Similarly, an NBFC-MFI starting at ₹5 crore (or ₹2 crore in the North-Eastern Region) must increase to ₹7 crore (or ₹5 crore in the North-Eastern Region) by March 31, 2025, and then to ₹10 crore.

If an NBFC fails to meet these NOF levels within the given time, it risks losing its registration as an NBFC.

Prudential Regulation

NBFCs, except for certain types, should maintain a leverage ratio of no more than seven. This ratio compares their total outside liabilities to their owned funds. For NBFCs focusing on gold jewelry loans, they need to keep a minimum Tier 1 capital of 12% of their risk-weighted assets. This includes both on-balance sheet and off-balance sheet items. They must also follow specific guidelines for handling deferred tax assets and liabilities.

Accounting Standards

NBFCs must prepare their financial statements according to Indian Accounting Standards if required. These standards are notified by the Government of India. They should also adhere to additional regulatory guidance. Other NBFCs should follow notified Accounting Standards, provided they don’t conflict with these directions.

Accounting for Investments

Investments are categorized for valuation purposes. For quoted current investments, they are valued at the lower of cost or market value. Unquoted equity shares are valued at cost or breakup value, whichever is lower. However, NBFCs can use fair value if necessary. Investments in unquoted government securities or bonds are valued at carrying cost. The valuation of mutual fund units and commercial papers follows specific guidelines.

Income Recognition

Income recognition is based on recognized accounting principles. Income from non-performing assets is recognized only upon actual realization. Interest income on loans with a moratorium can be recognized on an accrual basis if the account remains ‘standard’.

Income from Investments

Income from dividends, bonds, debentures, and government securities is recognized based on certain conditions. For example, dividend income from corporate bodies is recognized on an accrual basis when declared and the right to receive payment is established.

Asset Classification

NBFCs classify their assets into standard, sub-standard, doubtful, and loss assets. This classification depends on repayment performance and other factors. An asset’s classification can change based on its performance after rescheduling.

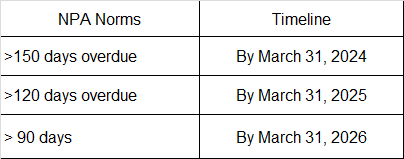

A glide path is provided to applicable NBFCs to adhere to the 90 days NPA norm as under:

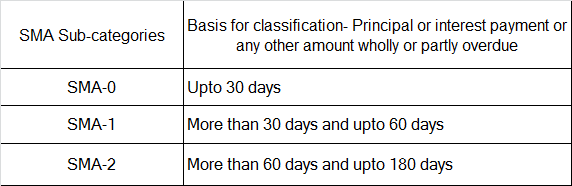

NBFCs shall recognize incipient stress in loan accounts, immediately on default, by classifying such assets as special mention accounts (SMA) as per the categories specified below:

Consumer Education on SMA/NPA

NBFCs should educate their customers about the concepts of overdue dates, special mention accounts (SMA), and non-performing asset (NPA) classification. This information should be available on their websites and in branches.

Provisioning Requirements

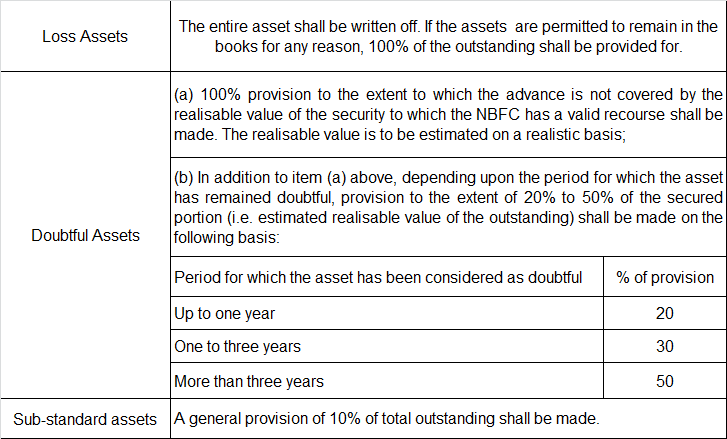

NBFCs must make provisions against sub-standard, doubtful, and loss assets. The amount of provision depends on the type of asset and its performance. For example, loss assets require 100% provisioning. Hire purchase and leased assets have specific provisioning requirements.

The provisioning requirement in respect of loans, advances and other credit facilities including bills purchased and discounted shall be as under:

Standard Asset Provisioning

NBFCs must make a provision of 0.25% for standard assets. This provision should be shown separately in the balance sheet.

Projects under Implementation

For on-going projects, NBFCs must follow specific guidelines, including those for projects in the commercial real estate sector.

Resolution of Stressed Assets

NBFCs with significant assets must follow the Prudential Framework for Resolution of Stressed Assets. This includes guidelines for restructuring and resolving stressed assets.

Investment Policy

NBFCs’ Boards must frame and implement an investment policy. This policy should classify investments and outline procedures for inter-class transfers.

Accounting Year

NBFCs must prepare their balance sheet and profit and loss account annually as of March 31. They must finalize these within three months of the year-end.

Disclosures in Financial Statements

NBFCs must disclose specific information in their financial statements. This includes provisions for bad debts and investment depreciation. These disclosures are in addition to other legal and regulatory requirements.

Policy on Demand/Call Loans

NBFCs must have a policy for demand or call loans. This policy should cover interest rates, repayment terms, and review procedures.

Regulatory Restrictions and Limits

Credit and Investment Concentration Norms for NBFCs

NBFCs controlled by an NOFHC must not:

- Have any financial dealings (like giving loans or making investments) with the promoters, their group entities, or individuals linked to the promoter group or the NOFHC.

- Invest in the equity or debt instruments of any financial entities under the NOFHC.

- Buy equity in other NOFHCs.

For clarity, the terms ‘Promoter’ and ‘Promoter Group’ are defined in the “Guidelines for Licensing of New Banks in the Private Sector.”

Declaration of Dividends

NBFCs should follow these rules to declare dividends:

- The Board of Directors must consider the Reserve Bank’s findings on NPAs, any issues raised in the Auditor’s Report, and the NBFC’s long-term growth plans.

- Only NBFCs that have met certain conditions for the past three years can declare dividends. These include meeting minimum capital requirements, having a net NPA ratio of less than six percent, complying with section 45-IC of the RBI Act, 1934, and adhering to Reserve Bank regulations without any restrictions on declaring dividends.

- Eligible NBFCs can declare dividends up to a payout ratio of 50 percent. There’s no limit for eligible NBFCs that don’t use public funds and don’t have customer interaction.

- NBFCs not meeting the capital ratio or net NPA ratio requirements can declare dividends up to 10 percent payout ratio, provided they meet the minimum capital requirement and have a net NPA of less than four percent.

- The Board must ensure that the total dividend proposed does not exceed these guidelines. The Reserve Bank will not consider any special requests for dividend declaration.

- NBFCs declaring dividends must report the details to the Reserve Bank’s Regional Office within two weeks of the declaration.

Ceiling on IPO Funding

NBFCs can only finance up to ₹1 crore per borrower for subscribing to Initial Public Offers (IPOs). They can set stricter limits if they choose.

Loans against NBFC’s Own Shares

NBFCs are not allowed to give loans against their own shares.

Loans against Security of Shares

NBFCs with assets of ₹100 crore or more must:

- Maintain a Loan to Value (LTV) ratio of 50 percent when lending against listed shares. This ratio must be maintained at all times.

- Use only Group 1 securities as collateral for loans above ₹5 lakh meant for investing in capital markets.

- Report quarterly to stock exchanges about the shares pledged as loan collateral.

Loans against Gold Jewellery

NBFCs must:

- Keep a Loan-to-Value (LTV) Ratio of 75 percent or less for loans against gold jewellery.

- Not give loans against bullion, primary gold, or gold coins.

- Verify the ownership of gold jewellery for loans over 20 grams.

- Value the gold jewellery based on the average closing price of 22-carat gold over the past 30 days.

Auctions of Pledged Gold

- Auctions must be conducted in the same town or district where the loan was given.

- The reserve price for auctioned gold should not be less than 85 percent of the 30-day average price of 22-carat gold.

- NBFCs must provide details of the auction outcome to the borrower.

- Annual reports of NBFCs must include auction details.

Safety and Security Measures

NBFCs lending against gold jewellery must ensure proper security and storage facilities, including safe deposit vaults, at each branch.

Opening New Branches

NBFCs with over 1,000 branches need the Reserve Bank’s approval to open more. New branches must have adequate security and storage facilities for gold jewellery.

Governance Guidelines

Experience of the Board:

To ensure the effective management of NBFCs, at least one board member should have relevant experience working in a bank or NBFC.

Risk Management Committee:

NBFCs must establish a Risk Management Committee (RMC) at either the board or executive level. This committee’s role is to assess the overall risks faced by the NBFC, including liquidity risk, and report its findings to the board.

Loans to directors, senior officers, and relatives:

NBFCs must have a board-approved policy for granting loans to directors, senior officers, relatives of directors, and entities where directors or their relatives hold significant shares. The policy should specify a threshold for reporting such loans to the board. Additionally, NBFCs must disclose the aggregate amount of such sanctioned loans and advances in their Annual Financial Statement, following the provided template in Annex XI.

Appointment of Statutory Central Auditors/Statutory Auditors:

NBFCs must adhere to the guidelines outlined in the circular titled ‘Guidelines for Appointment of Statutory Central Auditors (SCAs)/Statutory Auditors (SAs) of Commercial Banks (excluding RRBs), UCBs and NBFCs (including HFCs)’ dated April 27, 2021, with any amendments made over time. However, non-deposit taking NBFCs with assets below ₹1,000 crore have the option to maintain their existing procedure.

Acquisition/Transfer of Control of NBFCs:

For any takeover or acquisition of control of an NBFC (with or without a change in management), or any change in the NBFC’s shareholding resulting in a transfer of more than 26 percent shareholding, prior written permission from the Reserve Bank is required. However, approval is not needed if shareholding exceeds 26 percent due to share buybacks or capital reduction approved by a competent court. In such cases, the Reserve Bank must be notified within one month.

Regardless of the above, NBFCs must continue to inform the Reserve Bank about any changes in their directors or management.

Application for prior approval for acquisition/transfer of control:

NBFCs should submit an application, on the company’s letterhead, for obtaining prior approval from the Reserve Bank. This application should include information about proposed directors/shareholders (as per Annex XII), sources of funds of the proposed shareholders, declarations regarding associations with unincorporated bodies accepting public deposits or companies with rejected CoR applications, absence of criminal cases against directors/shareholders, and a bankers’ report on the proposed directors/shareholders. These applications should be submitted to the Regional Office of the Department of Supervision of the Reserve Bank where the NBFC’s Registered Office is located.

Requirement of Prior Public Notice about change in control/management:

Before transferring ownership or control (with or without share sale), NBFCs must provide at least 30 days’ public notice, with the Reserve Bank’s prior permission. This notice should include details of the intended sale or transfer, transferee particulars, and reasons for the transaction. The notice must be published in a leading national and a leading local vernacular newspaper (covering the registered office location).

Investment from FATF non-compliant jurisdictions:

NBFCs must also comply with instructions specified in paragraph 8 of these directions regarding investments from FATF non-compliant jurisdictions.

Need for public notice before closure of Branch/Office by NBFC:

- NBFCs must give at least three months’ public notice in a leading national newspaper and a leading local vernacular newspaper (covering the branch/office location) before closing any of their branches/offices. This notice should include the purpose of closure and arrangements made for servicing depositors, etc.

Information with respect to change of address, directors, auditors, etc. to be submitted:

- NBFCs must promptly communicate any changes in their complete postal address, contact details, directors’ names and addresses, principal officers’ names and designations, auditors’ names and office addresses, and specimen signatures of authorized officers to the Regional Office of the Department of Supervision of the Reserve Bank within one month of the change.

Fair Practices Code

Fair Practices Code (FPC) is a set of guidelines that NBFCs with customer interactions should adhere to. These guidelines are meant to ensure transparency and fairness in their dealings with borrowers. Here are the key points of the Fair Practices Code:

Loan Applications and Processing:

- All communication with borrowers should be in a language they understand.

- Loan application forms should provide necessary information to enable borrowers to compare terms and conditions with other NBFCs.

- Acknowledgement of loan applications should be provided, along with an indication of the expected processing time.

Loan Appraisal and Terms/Conditions:

- NBFCs must provide written communication in a language understood by borrowers regarding the sanctioned loan amount, terms, conditions, and the annualized interest rate.

- Penalties for late repayment should be prominently mentioned in the loan agreement.

Penal Charges in Loan Accounts:

- Penalties for non-compliance with loan terms should be treated as ‘penal charges’ and not added to the interest rate.

- The quantum of penal charges should be reasonable and clearly disclosed in loan agreements and other relevant documents.

Notice of Changes in Terms and Conditions:

- Borrowers should be informed in advance, in a language they understand, about changes in terms, interest rates, and other charges.

Release of Property Documents:

- NBFCs must release original property documents within 30 days of full repayment. Borrowers can choose the location for document collection.

- Compensation should be provided for delays in releasing documents, and procedures should be in place for handling cases of borrower demise.

Reset of Floating Interest Rate:

- NBFCs must inform borrowers about possible interest rate changes due to external benchmarks and allow borrowers to switch to a fixed rate.

- Borrowers should have options to enhance EMI, extend tenor, or make prepayments.

General:

- NBFCs should not interfere in borrower affairs except as per loan terms.

- Transfer requests from borrowers should be responded to within 21 days.

- Harassment in loan recovery should be avoided, and staff should be trained to handle customer interactions appropriately.

Interest Rate Regulation:

- NBFCs must adopt an interest rate model, disclose interest rates to borrowers, and update rates when necessary.

Complaints About Excessive Interest:

- Internal principles and procedures should be established for interest rate determination.

- Transparent communication about interest rates should be maintained.

Repossession of Vehicles:

- NBFCs must have legally enforceable repossession clauses, and terms should be communicated clearly to borrowers.

Lending Against Gold Jewellery:

- NBFCs should have a Board-approved policy for lending against gold, including proper due diligence, safe storage of jewellery, and transparent auction procedures.

Loan Facilities for Physically/Visually Challenged:

- NBFCs should not discriminate against physically/visually challenged applicants.

- Training programs should include modules on the rights of disabled persons, and grievances should be addressed through established mechanisms.

Miscellaneous Instructions

Opening of Branch/Subsidiary/Joint Venture/Representative Office or Undertaking Investment Abroad by NBFCs

In addition to the Foreign Exchange Department (FED) of the Reserve Bank’s rules for overseas investment, Non-Banking Financial Companies (NBFCs) must follow these instructions. NBFCs need the Reserve Bank’s prior approval for opening branches, subsidiaries, joint ventures, representative offices, or making investments abroad. Applications for No Objection will be evaluated based on general and specific conditions.

General conditions include:

- Investments are not allowed in non-financial service sectors.

- Direct investment in activities banned under FEMA or in sectoral funds is prohibited.

- Investments are only permitted in entities regulated by a financial sector regulator in the host country.

- The total overseas investment must not exceed 100% of the Net Owned Funds (NOF). Investment in a single entity, including its stepdown subsidiaries, should not be more than 15% of the NBFC’s owned funds.

- Overseas investment should not involve complex, multi-layered structures. Only one intermediate holding entity is allowed.

- The NBFC’s Capital to Risk (Weighted) Assets Ratio (CRAR)/leverage should meet regulatory requirements after the investment.

- The NBFC must maintain the required level of NOF after accounting for the proposed investment.

- Net Non-Performing Assets should not exceed 5% of net advances.

- The NBFC should have been profitable for the last three years with satisfactory performance.

- Compliance with FEMA regulations is mandatory.

- Regulatory compliance and servicing of public deposits must be satisfactory.

- Compliance with Know Your Customer (KYC) norms is required.

- Special Purpose Vehicles (SPVs) set up abroad or acquisitions will be treated as investments or subsidiaries/joint ventures, depending on the investment percentage.

- An annual certificate from statutory auditors confirming compliance with these directions is required.

- The Reserve Bank may withdraw permission if any adverse features are noticed.

Specific conditions include:

Opening of Branch Abroad: Generally, NBFCs are not allowed to open branches abroad. Those already having branches can continue, subject to compliance.

Opening of Subsidiary Abroad: The same conditions apply as for opening a branch. The Reserve Bank’s No Objection Certificate (NoC) is independent of overseas regulators’ approval. Additional stipulations include:

- The parent NBFC cannot extend implicit or explicit guarantees to such subsidiaries.

- Requests for letters of comfort in favor of the subsidiary from Indian institutions are not permitted.

- The NBFC’s liability in the overseas entity is limited to its equity or fund-based commitment.

- The subsidiary should not be a shell company. However, companies engaged in financial consultancy and advisory services with no significant assets are not considered shell companies.

- The subsidiary should not be used for raising resources for Indian operations.

- The parent NBFC must obtain and make available to the Reserve Bank periodic reports/audit reports on the subsidiary’s business.

- If the subsidiary is inactive or reports are not provided, the approval may be reviewed or recalled.

- The subsidiary must disclose in its Balance Sheet that the parent entity’s liability is limited to its equity or fund-based commitment.

- The subsidiary’s operations are subject to regulatory prescriptions of the host country.

- Joint Ventures Abroad: Investments in joint ventures are governed by the same guidelines as subsidiaries.

Opening of Representative Offices Abroad: Representative offices abroad can only engage in liaison work, market study, and research without any fund outlay, provided they are regulated in the host country. Periodic reports on the representative office’s business are required.

Expansion of Activities of NBFCs through Automatic Route: NBFCs with Foreign Direct Investment (FDI) under the automatic route can only undertake activities permissible under this route. Diversification requires prior approval from the Foreign Investment Promotion Board (FIPB). Companies diversifying into the NBFC sector must comply with minimum capitalization norms and other regulations.

Managing Risks and Code of Conduct in Outsourcing of Financial Services by NBFCs: NBFCs must assess their existing outsourcing arrangements to align with instructions in Annex XIII.

Guidelines on Digital Lending: NBFCs must follow the circular on ‘Guidelines on Digital Lending’ dated September 02, 2022, and subsequent amendments.

Guidelines on Default Loss Guarantee (DLG) in Digital Lending: NBFCs must adhere to the circular on ‘Guidelines on Default Loss Guarantee (DLG) in Digital Lending’ dated June 08, 2023, and subsequent amendments.

Loans Sourced by NBFCs over Digital Lending Platforms: Adherence to Fair Practices Code and Outsourcing Guidelines: NBFCs engaging digital platforms for loan provision must adhere to the Fair Practices Code and regulatory instructions on outsourcing financial and IT services. Key points include:

- Disclosure of digital lending platforms acting as agents on the NBFC’s website.

- Digital lending platforms must disclose the NBFC’s name to customers.

- Issuance of sanction letters on the NBFC’s letterhead.

- Provision of loan agreement copies and related documents to borrowers.

- Effective oversight and monitoring of digital lending platforms.

- Creation of awareness about grievance redressal mechanisms.

- Violations will be taken seriously.

Credit Default Swaps (CDS) – NBFCs as Users: NBFCs can only participate in the CDS market as users, buying credit protection to hedge credit risk on corporate bonds they hold. They cannot sell protection or enter into short positions in CDS contracts. Exiting bought CDS positions must be done by unwinding with the original counterparty or assigning them to the buyer of the underlying bond. Compliance with operational requirements for CDS in Annex XIV is mandatory.

Currency Futures: NBFCs can participate in designated currency futures exchanges recognized by SEBI as clients, only for hedging underlying forex exposures. Disclosures in the balance sheet regarding currency futures transactions must align with SEBI guidelines.

Interest Rate Futures: NBFCs can participate in designated interest rate futures (IRF) exchanges recognized by SEBI as clients, adhering to the ‘Rupee Interest Rate Derivatives (Reserve Bank) Directions, 2019’ for hedging underlying exposures. Data submission on IRF participation is required semi-annually to the Reserve Bank’s Regional Office.

- Transactions in Government Securities: NBFCs can undertake transactions in Government securities through various accounts as permitted by the Reserve Bank.

- Operative Instructions Relating to Government Securities Transactions: NBFCs must follow guidelines on transactions in Government securities as outlined in relevant circulars and the Repurchase Transactions (Repo) (Reserve Bank) Directions, 2018.

- Reporting Platform for Corporate Bond Transactions: NBFCs must report secondary market OTC trades in corporate bonds within 15 minutes on stock exchanges (NSE, BSE, MCX-SX). Compliance with the circular ‘FIMMDA’s Trade Reporting and Confirmation platform for OTC transactions in Corporate Bonds and Securitized Debt Instruments’ is required.

- Raising Money through Private Placement by NBFCs: NBFCs must follow guidelines on private placement of Non-Convertible Debentures (NCDs) in Annex XV. Provisions of the Companies Act, 2013, apply where not contradictory.

- Entry into Insurance Business: NBFCs seeking to enter the insurance business must apply to the Reserve Bank’s Regional Office with necessary details certified by statutory auditors. Insurance agency business can be undertaken on a fee basis without risk participation.

Introduction to RBI – NBFC Scale Based Regulation

Regulations applicable for NBFC-ML

Regulatory Instructions for NBFC-UL

Directions for NBFC – Micro Finance MFIs

Specific Directions for NBFC-Factors and NBFC-ICCs

Specific Directions for Infrastructure Debt Funds IDFs-NBFC

Scoring Methodology for Identification of NBFC as NBFC-UL

Regulatory Guidance on Implementation of Ind AS by NBFCsv

Norms on Restructuring of Advances by NBFCs

Early Recognition of Financial Distress

Flexible Structuring of Long Term Project Loans to Infrastructure and Core Industries

Guidelines on Liquidity Risk Management Framework

Disclosures in Financial Statements – Notes to Accounts of NBFCs

Managing Risks and Code of Conduct in Outsourcing of Financial Services by NBFCs

Guidelines for Credit Default Swaps – NBFCs as Users

Guidelines on Private Placement of NCDs by NBFCs

Guidelines for Entry of NBFCs into Insurance

Guidelines on Issue of Co-Branded Credit Cards

Guidelines on Distribution of Mutual Fund Products by NBFCs

Guidelines on Perpetual Debt Instruments

Guidelines on Liquidity Coverage Ratio (LCR)

Balance Sheet Disclosure Guidelines for NBFCs in Middle Layer and Above

Self-Regulatory Organization (SRO) for NBFC-MFIs – Criteria for Recognition

{kind=link}