Additional reporting by Multinational companies – Transfer pricing

- The OECD had devised many action plans to combat BEPS. OECD also recommended a three-tier documentation approach for transfer pricing under Action Plan 13.

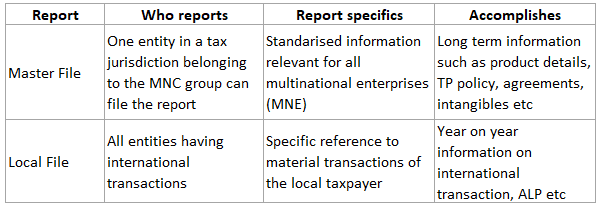

Three tier documentation

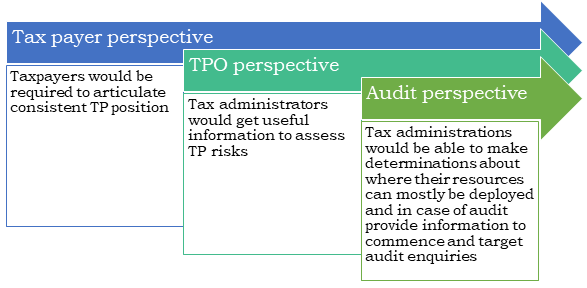

Advantages of three tier reporting

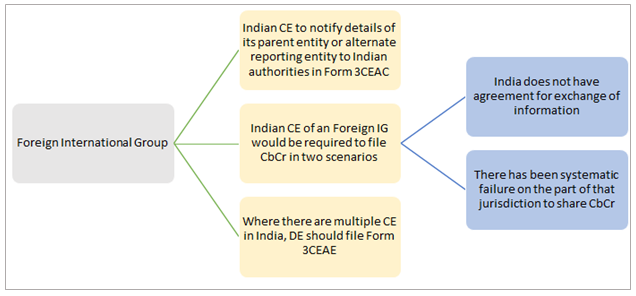

- Elements of CbC and Master File reporting requirement and related matters have been incorporated in the Section 286 of the Act.

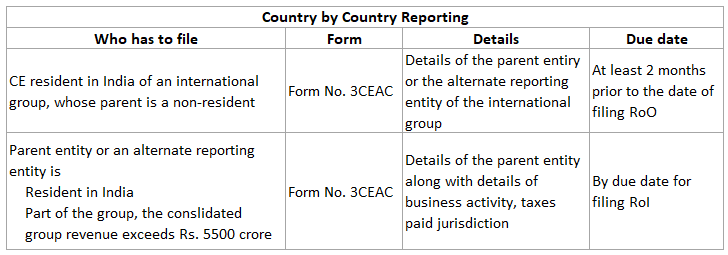

- This reporting shall be applicable in respect of an international group for an accounting year if the total consolidated revenue as reflected in the CFS for the accounting year preceding year is above the threshold limit.

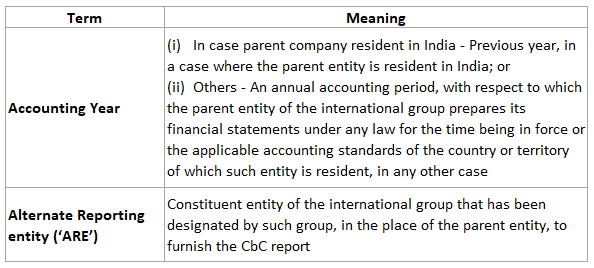

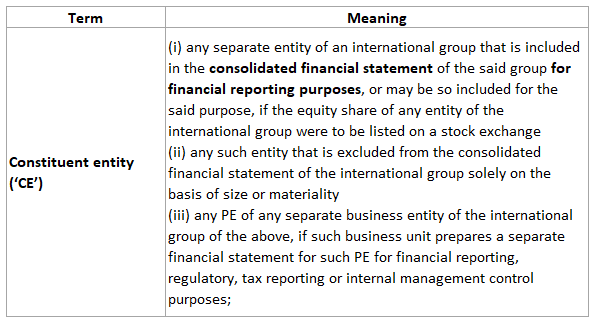

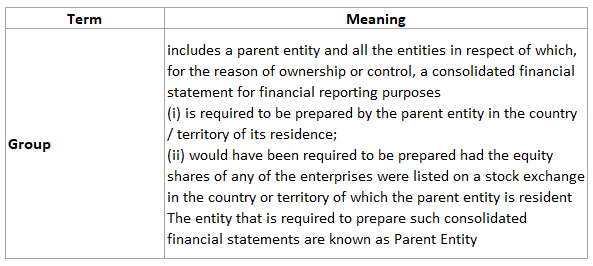

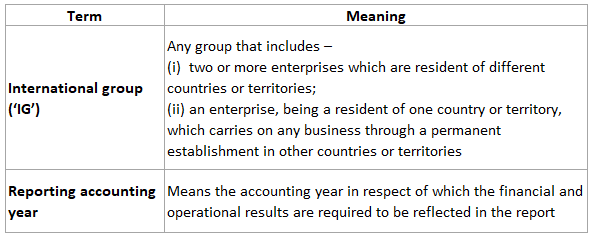

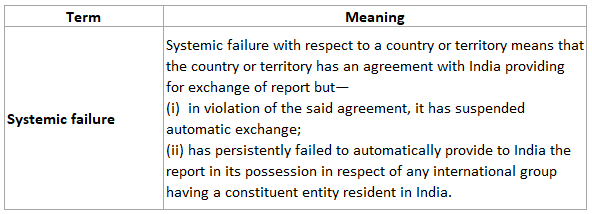

Key terms to understand

- There are certain terms which are repeatedly used in this section.

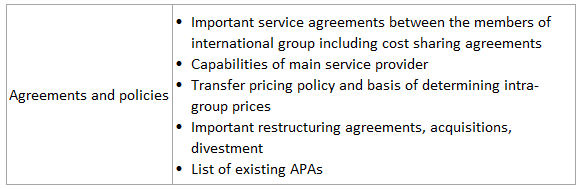

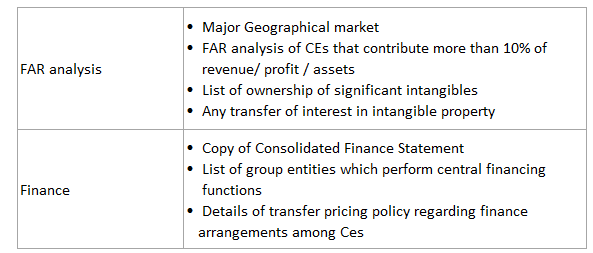

Significant aspects of Master File

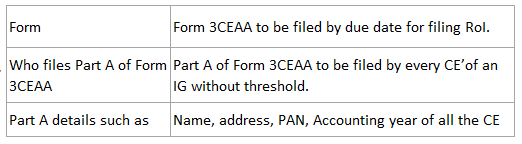

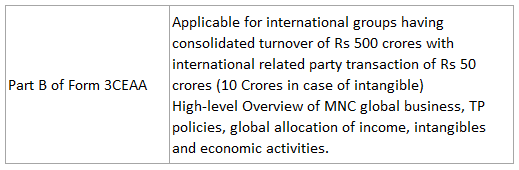

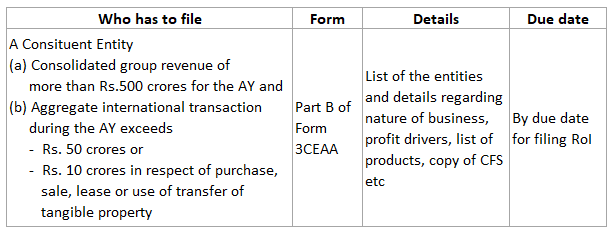

- If an entity is CE of a IG, then Part A of Form 3CEAA which contains minimum disclosures are mandatory. If the IG’s consolidated turnover exceeds Rs 500 crore, then filing of Part B becomes mandatory if the international transaction of the CE exceeds certain threshold.

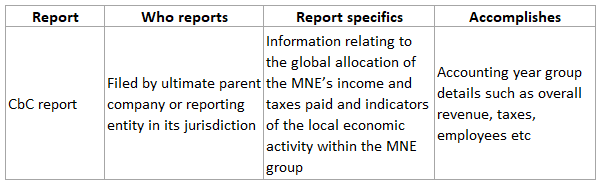

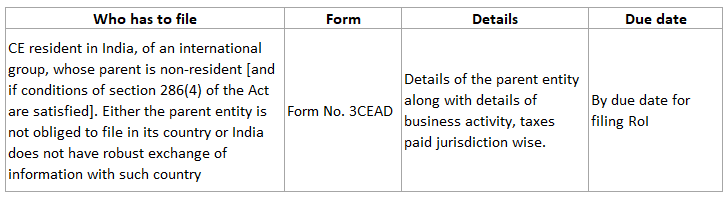

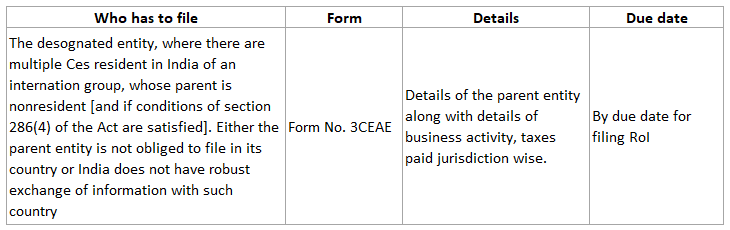

Country by Country Reporting (‘CbCr’)

- The rate of exchange for the calculation of the value in rupees of the consolidated group revenue in foreign currency shall be the telegraphic transfer buying rate of such currency on the last day of the accounting year

- “Telegraphic transfer buying rate” shall have the same meaning as assigned in the Explanation to rule 26;

Contents in Master File and CbCr

- As the name suggests the contents of the Master file are not likely to change very rapidly and provides the direction and long term planning of the international group.

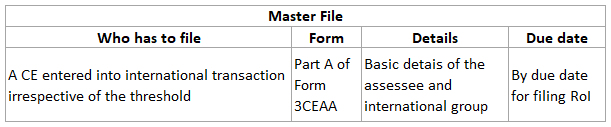

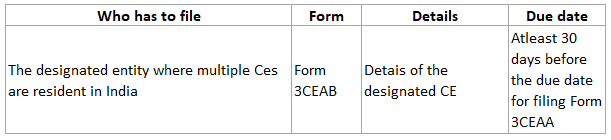

- Part A of the Form 3CEAA (which has to be complied by every CE in India which part of the International group) contains basic details such as Name, address, Tax identification number, accounting year of the international group, number of CEs operating in India and their details

- Part B contains further details which is applicable if the consolidated turnover exceeds Rs 500 crores and international transaction of the CE

- Exceeds Rs 50 crores; or

- Aggregate value of international transaction is more than Rs.10 crores in respect of purchase, sale, transfer, lease, or use of intangible property

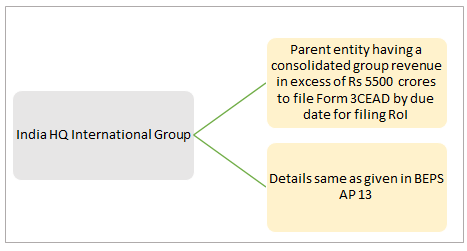

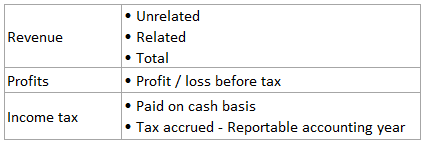

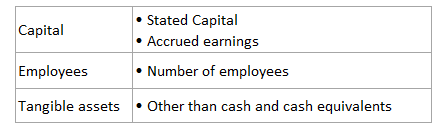

- Contents of CbC Report provide a snapshot of the financial performance, employment details of the international year during the relevant accounting year. While master file provides the policy decisions of the group, the CbCr would give an idea how the policies have been implemented and the business results for the accounting year. CbC reports details in a tabulated form.

- Apart from the details such as name, Address, PAN of reporting entity, the form also require confirmation if the reporting company is the parent company. The form has two parts namely

- Part A: Allocation of income, taxes and business activities by tax jurisdiction

- Part B: List of all CEs of the IG included in each aggregation per tax jurisdiction

- Tax jurisdiction wise details of

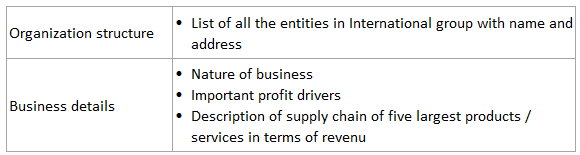

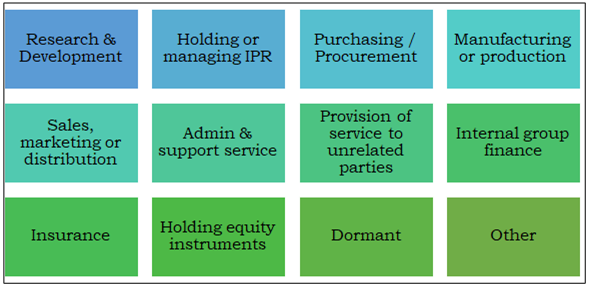

- Part B requires information regarding the main business activities classified in a particular format for each CE. The business activity classification is as under

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing