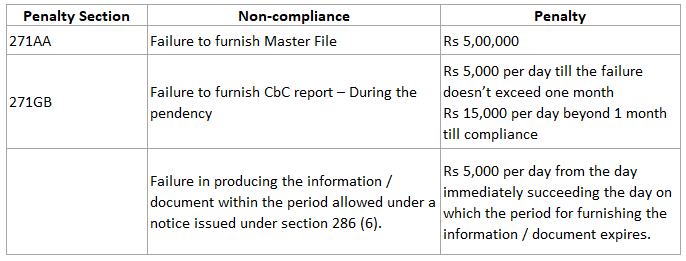

Penalties for non-compliance – Transfer Pricing

- The Act has prescribed strict penalties for non-compliance in terms of non-disclosure or incorrect disclosure

Question

International group shall maintain information and documents in Master file when Consolidated group revenue of the International group is (as reflected in Consolidated Financial Statements of the International Group) is

- More than Rs.500 crores

- More than 5500 crores

- More than Rs 50 crores

Answer a.

International group shall maintain information and documents in Master file when Consolidated group revenue of the International group is (as reflected in Consolidated Financial Statements of the International Group) is Rs 500 crores. The form contains Part A and Part B. Part A is mandatory for the CE who fulfills the turnover threshold and Part B would be applicable for the CEs who satisfies additional conditions regarding international transactions.

Question

Master file shall be filed in form 3CEBB part B of form 3CEAA needs to be filed by constituent entity of international group when

- Consolidated group revenue of the international group is more than Rs.500 crores and aggregate value of international transaction is more than Rs.50crores

- Consolidated group revenue of the international group is more than Rs. 500 crores and aggregate value of international transaction is more than Rs.10 crores in respect of purchase, sale, transfer, lease, or use of intangible property

- Both a and b

- None of the above

Answer c.

Compliance would be triggered if cconsolidated group revenue of the international group is more than Rs.500 crores and aggregate value of international transaction is more than Rs.50 crores or aggregate value of international transaction is more than Rs.10 crores in respect of purchase, sale, transfer, lease, or use of intangible property

Question

Avary India Ltd is a resident constituent entity of an international group. Its parent entity, Amaze International is resident of country Y. Amaze International furnished CbC report in country Y and country shared the details with Indian Tax authorities. In this case, Avary India Ltd;

- Has to file CbCr if the consolidated revenue of the group exceeds Rs 5500 crores

- Has to file CbCr if the consolidated revenue of the group exceeds Rs 500 crores

- Does not have to file CbCr

Answer c.

Since Amaze international has already filed the CbCr in the country of residence and the country has shared the details with India, there is no need to file CbCr by Avary India Ltd.

Question

Avary India Ltd is a resident constituent entity of an international group. Its parent entity, Amaze International is resident of country Y. Avary India Ltd is required to furnish CbC report if

- India does not have an arrangement for exchange of CbC report

- Country Y is not exchanging information with India even though there is an agreement (existence of systematic failure)

- Either a. or b.

Answer c.

There are other reasons too. Avary India Ltd is required to furnish CbC report if India does not have an arrangement for exchange of CbC report or Country Y is not exchanging information with India even though there is an agreement (existence of systematic failure)

Question

Regarding Master file, if there are multiple Constituent Entities (CEs) in India, then the CE should intimate the details of the Designated Entity (‘DE’) to the tax officer in which form and when?

- Form 3CEAA and atleast 2 months before the due date for filing Return of Income

- Form 3CEAB and atleast 30 days before the due date for filing Return of Income

- All the CEs have to file Master file in Form 3CEAA

Answer b.

All the CEs should intimate the details of the designated entity to the DGIT(RA) in Form 3CEAB and atleast 30 days before the due date for filing Return of Income

Question

Details of profit earned and taxes paid for the accounting year by the international group and tax jurisdiction-wise details of main business activity is to be provided in

- Master file

- Country by Country Report

- Local file

Answer b.

While master file provides the policy decisions of the group, the CbCr would give an idea how the policies have been implemented and the business results for the accounting year. Details such as profits earned and taxes paid including classification of business activity is provided in CbCr

Question

Trinity Software is required to furnish report under CbC provisions but it filed such report after 35 days from the due date. The amount of penalty shall be

- Rs 17,50,000

- Rs 2,25,000

- Rs 1,75,000

Answer b.

For the first 30 days the penalty would be Rs 5000 per day which would amount to Rs 150,000 . The next 5 days would carry a penalty of Rs 15,000 per day which amounts to Rs 75,000 . The total penalty would be Rs 225,000 [150,000+75,000]

Question

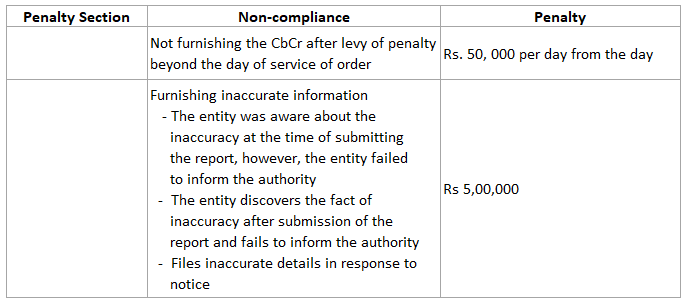

If an Entity is required to furnish report under CbC provisions but it failed to file such report even after service of penalty order. The amount of penalty shall per day would be

- Rs 5,000 per day of default

- Rs 15,000 per day of default

- Rs 50,000 per day of default

Answer c.

Not furnishing CbC report even after levy of penalty is Rs 50,000 per day of default

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing