Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Introduction

- In the past few decades, the world has seen large movement of capital and investment from developed and developing countries.

- This has resulted in huge economic development, boosted trade and increases foreign direct investment in various countries.

- Many developing countries (low – cost locations) saw boon in their manufacturing activity and become operation hub for many MNEs.

- This also accelerated growth, innovation and created jobs.

- Taxes are the main revenues for the economy. Once cross border activities increased, there were many instances of double-taxation and need to eliminate the same was noticed.

- Progressively, Governments entered bilateral tax agreements often called as Double Taxation Avoidance Agreements (‘DTAA”) with other countries for elimination of double taxation and resolution of disputes.

- The global MNEs started adopting sophistication in tax planning thereby reducing the overall tax burden of the MNE.

- Sometimes these tax planning methods were very aggressive, touching the boundaries of exploiting legal arbitrage which often leads to Base Erosion and profit shifting (‘BEPS’).

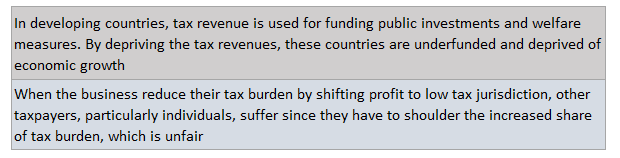

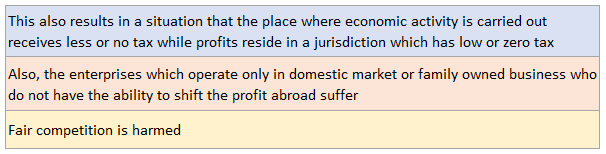

Adverse effect of BEPS

- BEPS refers to tax planning that exploit gaps in the domestic laws and mismatches in tax rules to make profit disappear for tax purposes or to shift profits to locations where there is little or no economic activity but the taxes are low. This has adverse effect on the economy for many reasons including:

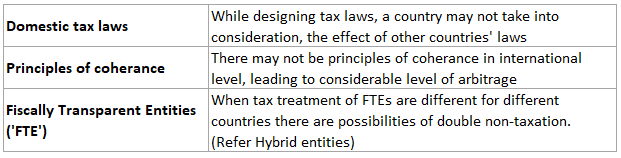

Why there is disparity?

- Taxation is the core of a country’s sovereignty. These domestic tax laws of each country lead to gaps and mismatches which are broadly discussed below:

BEPS action plan

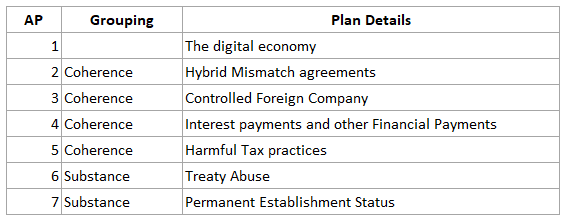

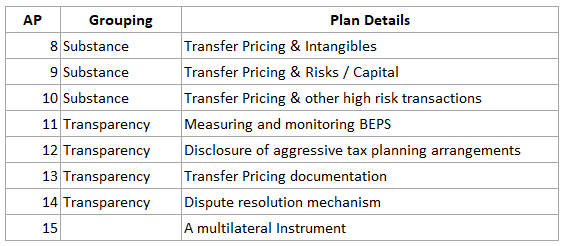

- The OECD published a report addressing the BEPS issues by publishing draft Action Plans (‘AP) in July 2013 which came to finality in October 2015.

- It has 15 APs to address BEPS in a comprehensive manner and set a deadline for implementation.

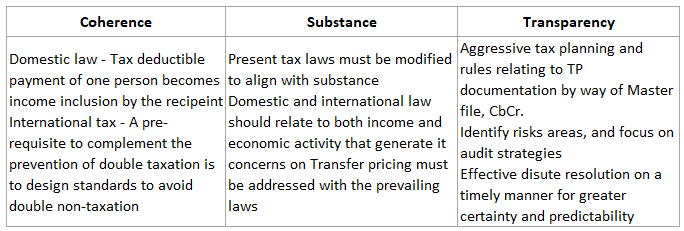

- The action plans are based on three main principles:

BEPS overview of Action Plan

Question

Why there is often tax arbitrage between countries?

- Domestic laws may not take in to account the effect of its laws on other countries and lack of coherence and differential tax treatment may cause tax arbitrage

- Tax arbitrage happens when MNEs try to evade taxes

- Tax arbitrage happens because countries want to preserve its tax sovereignty

Answer a.

Question

In the context of BEPS, what is meant by coherence?

- Domestic and international law should relate to both income and economic activity that generate it

- Identifying risks areas, and focus on audit strategies between taxing countries

- Tax deductible payment of one person becomes income inclusion by the recipient and thereby preventing double non-deduction

Answer c.

Coherence means tax deductible payment of one person becomes income inclusion by the recipient which is taken care in domestic law and may be difficult to practice in international law thereby paving way for double non-deduction.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing