Limitation of interest deductions – transfer pricing

Introduction

- Popularly known as ‘Thin Capitalization Rules’, this provision intends to cap the interest that can be paid to the AEs in case of borrowings.

- Generally, debt is a preferred instrument to provide funds to the subsidiary or group company rather than equity due to the fact that interest on debt is a deductible expenditure for tax and there would be regular cash flow to the lender as well.

- The DTAAs also provide a favourable tax rate for the interest earned by the non-residents

- High leverage and excess interest deductions erodes the profitability of the payee. Normally such huge debt would not be possible from a third party as highly leveraged company would find it difficult to raise loans more so at a favourable rate. So normally, the AEs instead of providing funding by means of equity, often structure it as debt.

India response

- India introduced section 94B to the effect that “that interest expenses claimed by an entity to its associated enterprises shall not be deductible in computation of income under the “Profits and gains of business or profession” to the extent that it arises from excess interest.”

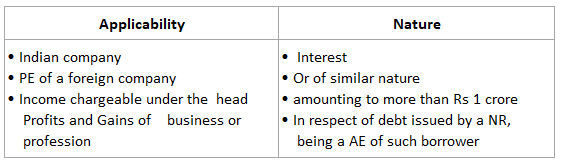

- Section 94B is non-obstinate clause which states that where an Indian company, or a PE of a foreign company in India, being the borrower, incurs any expenditure by way of interest or of similar nature exceeding one crore rupees which is deductible in computing income chargeable under the head “Profits and gains of business or profession” in respect of any debt issued by a non-resident, being an associated enterprise of such borrower, the interest shall not be deductible in computation of income under the said head to the extent that it arises from excess interest.

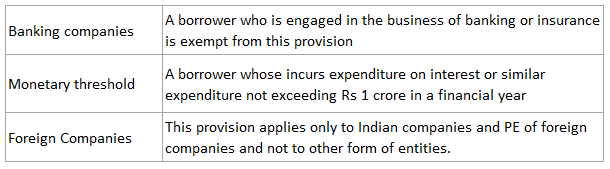

- Budget 2020 has proposed to amend section 94B by inserting sub section (1A) to the effect that the provisions of deemed AE would not apply if the lender is an Indian PE of a non-resident who is engaged in the banking business. Consequently, interest paid to such lenders would not fall under the purview of 94B and would escape disallowance.

Applicability

- So conditions for attracting section 94B are summarized as:

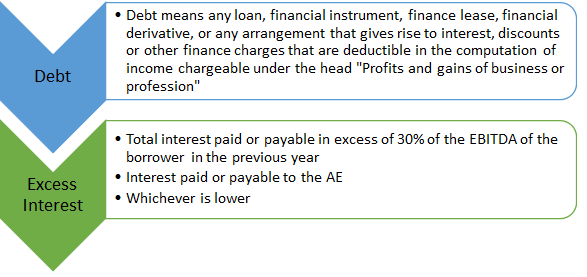

Meaning of important terms

Types of Debts

Key aspects

Question

ABC LLP, a partnership firm has made provision towards interest on loan to its group entity. The EBITDA is Rs 100 crores and interest payment of AE is 40 crores. What amount would be disallowed u/s 94B?

- Excess interest is Rs 10 crores since it is excess of interest over 30% of EBITDA.

- Excess interest is Rs 40 crores since entire AE interest is disallowed

- No excess interest.

Answer c.

Section 94B is applicable only for companies and not for partnership firm so there is no interest deduction disallowance

Question

Amtex India has obtained a loan of Rs 150 crore from HSBC, Singapore. Amtex USA has placed as deposit of Rs 100 crore with HSBC Singapore. Which statement is true.

- There is no limitation in interest deduction since HSBC Singapore is not an AE of Amtex India

- There would be limitation in interest deduction since HSBC Singapore is a Non-resident

- There would be limitation in interest deduction since Amtex USA has placed a deposit with HSBC Singapore is a Non-resident

- There would be no limitation in interest deduction since Amtex USA since the deposit is not corresponding and matching

Answer d.

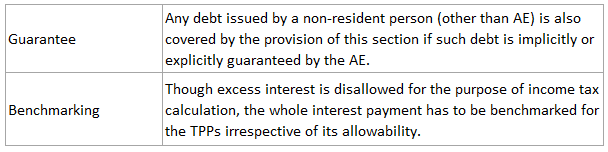

Debt issued by a lender which is not associated but an associated enterprise either provides an implicit or explicit guarantee to such lender or deposits a corresponding and matching amount of funds with the lender would also covered under section 94B and interest limitation would apply. Since the there is no matching deposit (Rs 150 crore debt but Rs 100 crore deposit), section 94B would not apply.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Penalties for non-compliance – Transfer Pricing