International Transaction – Transfer Pricing

- Transfer pricing provisions are applicable to determine the arm’s length price of international transaction and specified domestic transaction. Though, specified domestic transactions are also part of the transfer pricing provisions, it predominantly deals with international transaction. Therefore, it is essential to understand the term which is provided in Section 92B (1)

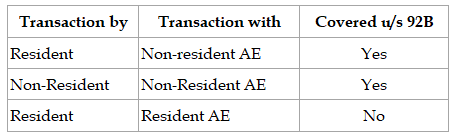

Transaction between two or more AEs either or both are NRs.

Summary

Question

Which of the following is an international transaction?

- Nippon USA purchases goods from Nippon Japan amounting to $1 million

- Interest of Rs 10 crores paid by K Ltd (India) to Singapore branch of HSBC Bank

- K India purchases spare parts from its subsidiary P India Ltd amounting to Rs 2 lakhs

- Indian branch of R USA paying royalty to R Singapore (WOS of R USA) amounting to USD 10 million.

Answer d.

It is an international transaction. Both are AEs and both are non-residents and Indian branch of the non-resident which has business connection in India is paying the royalty.

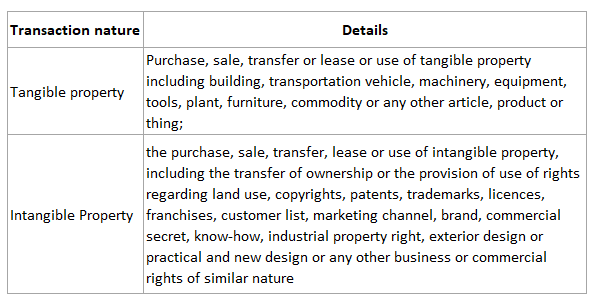

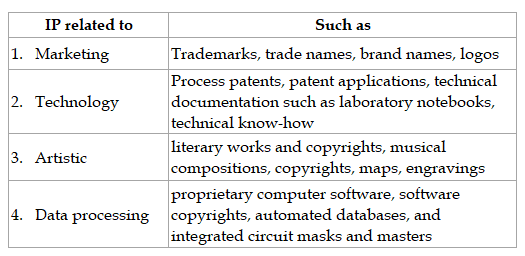

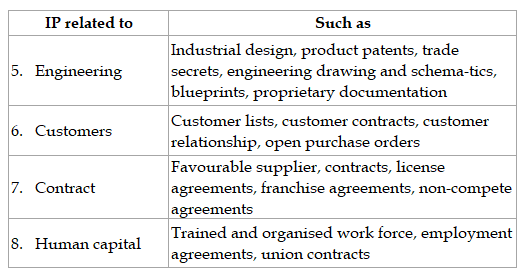

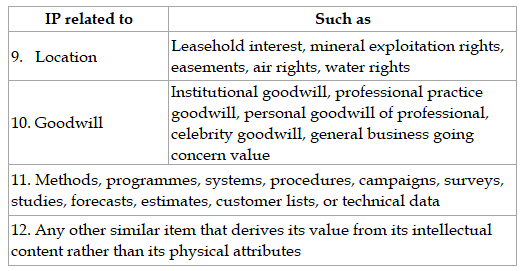

Intangible property (‘IP’):

The term intangible property includes

- To understand what constitutes an ‘International transaction’, we need to understand what ‘Transaction’ is. Section 92F defines the term ‘Transaction’ to include an arrangement, understanding or action in concert

- Whether or not such arrangement, understanding or action is formal or in writing; or

- Whether or not such arrangement, understanding or action is intended to be enforceable by legal proceeding.

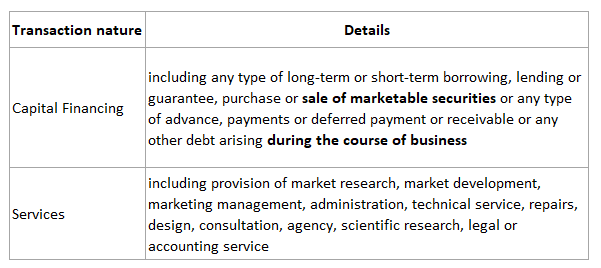

Financing transaction

- It was litigated whether receipt of security premium below market value in respect of issue of shares would be regarded as International transaction in the case of Vodafone India Services (P) Ltd vs UOI 50 Taxmann.com 300 (Bombay).

- Vodafone India offered shares at a premium of Rs 8509 ( Face value of Rs 10) per share to its parent company. However, the AO and the TPO contended that the share premium ought to have been Rs 53,775 and treated the difference as income in the hands of the assessee.

- It was held in the court as follows:

- The activity of issue of shares to AE at a price below the FMV does not give rise to any income. There should be income arising from international transaction on application of TP provisions

- Income will not include capital receipts, unless such receipts are specifically covered. The share premium is a capital amount and cannot come within the purview of international transaction CBDT’s instruction No.2/2015 dated 29-01-2015

- CBDT had also accepted the judgement of Bombay High Court and did not appeal further. So this the settled position now.

Question

HML India issued 10,000 shares at Rs.110 (face vale of Rs.10 each) at a premium of Rs.100 per share to its holding company, R International. Choose the correct statement

- Transfer pricing provisions would not be applicable on such transaction irrespective of the market value of shares

- Transfer pricing provisions would be applicable on such transaction when the fair market value of share is Rs.150 per share.

- Transfer pricing provisions would be applicable on such transactions when the fair market value of shares is Rs.90 per share

Answer a.

Based on the Vodofone ruling by Bombay HC, the activity of issue of shares to AE at a price below the FMV does not give rise to any income. There should be income arising from international transaction on application of TP provisions.

Deemed International Transaction – Section 92B(2)

- Where in respect of a transaction entered into by an enterprise with a person other than an AE (‘Other Person’)

- There exists a prior agreement in relation to the relevant transaction between the other person and the AE

- Where the terms of the relevant transactions are determined in substance between such other person and the AE and

- Either the enterprise or the AE or both of them are NRs

- Then such transaction entered into between the enterprise and the other person shall be deemed to be an international transaction entered in between AEs whether or not such other person is a NR.

Example

- Let us say that A India Ltd (‘A’) has an AE B US Inc (‘B’). B has entered into a contract with C India Ltd (‘C’) for supply of certain laptops to all its subsidiaries across the world. Pursuant to that contract, if A purchases laptop from C, then that transaction would be deemed to be an international transaction. In this example, it is immaterial if C is a resident or a non-resident until either A or B or both are non-resident.

Question

A Ltd (India) is the subsidiary of AB International (USA). A Ltd import certain goods from B international (Singapore), independent third party. There exists a prior agreement between B International and AB International (USA) for import of such goods. Such transaction of import from third party:

- Shall not be deemed to be an international transaction as both parties (i.e. A Ltd and AB International) are not associated enterprises

- Shall be deemed to be an International transaction even of transaction is made with Independent third party

- None of the above

Answer b. Where in respect of a transaction entered into by an enterprise with a person other than an AE (‘Other Person’), there exists a prior agreement in relation to the relevant transaction between the other person and the AE, Where the terms of the relevant transactions are determined in substance between such other person and the AE and either the enterprise or the AE or both of them are NRs, then it would be regarded as deemed international transaction

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing