Anti-Avoidance measures in certain jurisdictions – Transfer pricing

- Specific anti-avoidance measures in respect of transactions with persons located in Notified Jurisdictional area was introduced in the Act under sec 94A

- We have seen in earlier sections that transactions with the AEs are subject to transfer pricing provisions.

- This is generally sufficient to cover all the related party transactions, since most countries exchange information to the tax authorities of the other country.

- Where the exchange of information regarding the tax residence of a particular country is difficult to obtain, the CBDT had come up with the idea of Notified Jurisdictional Area (NJA) where any transaction with the resident of that country or jurisdiction would have to comply with transfer pricing provisions irrespective of whether the other entity is an AE or not.

- Further, rate of TDS was also prescribed for specified transactions with residents of NJA.

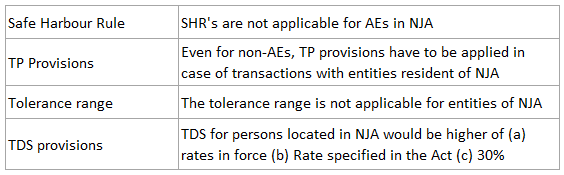

- Some significant features for NJA entities are

- CBDT had earlier in November 2013, notified Cyprus as NJA.

- However, after the negotiation of India – Cyprus treaty, this notification has been rescinded in December 2016.

Question

If a country is a Notified Jurisdictional Area, then

- SHRs do not apply for transactions with the AEs in that country

- Even for non-AEs, TP provisions have to be applied in case of transactions with entities resident of NJA

- The tolerance range is not applicable for entities of NJA

- All of the above

Answer d.

For a country identified as a Notified Jurisdictional Area, the beneficial SHRs are not applicable and even for non-AEs, TP provisions have to be applied in case of transactions with entities resident of NJA. Further tolerance range (3% / 1%) is not applicable for ALP for entities in NJA.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing