Determination of ALP – Transfer Pricing

- Rule 10C deals with the determination of most appropriate method. Under this Rule, the method is best suited to the facts and circumstances, and which provides the most reliable measure of ALP in relation to the international transaction will be considered to be the MAM. Factors that needs to be considered are:

- Nature or class of transaction

- The class or classes of AEs and FAR

- Availability and reliability of data

- Degree of comparability between the transactions

- Extent to which reliable and accurate adjustment can be made to account for the difference

- The nature, extent and reliability of assumptions required to be made in application of a method

- In case of international transaction or Specified Domestic Transaction (‘SDT’) undertaken on or after 01.04.2014 where more than one price is determined by the MAM, the ALP shall be computed in the prescribed manner specified in Rule 10CA.

When there are more than one Arm’s Length Price

- As per Rule 10CA(1), in such situations where in respect of an international transaction or SDT, the application of the MAM referred into section 92C(1) results in determination of more than one price, then, the ALP has to be computed on the basis of dataset constructed by placing such prices in an ascending order as provided in Rule 10CA(2).

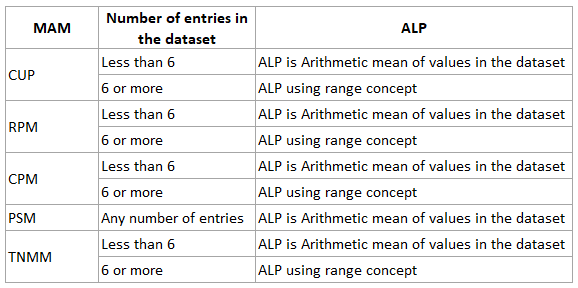

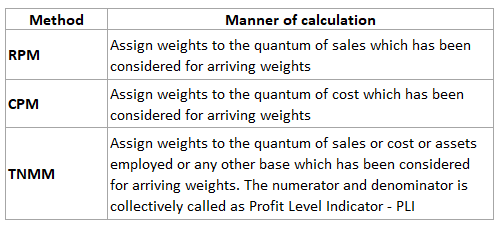

- The CBDT has issued rules for use of Multiyear data and range concept and would be applicable only in cases where RPM, CPM or TNMM has been selected as MAM.

- For each comparable, the data shall relate to the current year.

- If such data is not available at the time of furnishing the RoI, data pertaining to upto 2 preceding financial years may be used.

- If the current year is Y0, Previous year is Y1 and previous to that year is Y2, then the rules do not envisage use of data if only data of Y2 is available. Such comparable can be used only if Y0 and Y1 data are available. Similarly, if Y0 data is not comparable, then that data should be rejected.

- When using multi-year data, data for each comparable should be weighted average of the selected years.

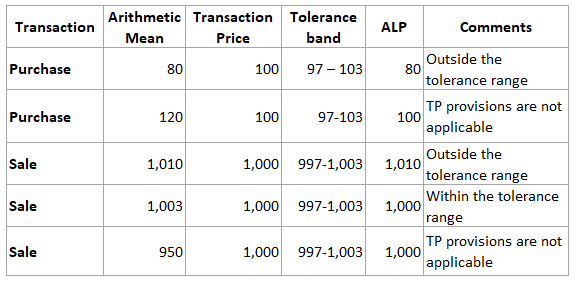

Use of tolerance band

- If there are fewer than 6 comparables, then arithmetic mean shall apply along with tolerance range benefit.

- The CBDT has notified that where the variation between ALP as determined under section 92C and the transaction price does not exceed 1% of the transaction price in case of wholesale trading and 3% on other cases, then the transaction price will be regarded as ALP.

- Wholesale trading means, transactions fulfilling following conditions, namely:

- Purchase cost of finished goods is 80% or more of the total cost pertaining to such trading activities; and

- Average monthly closing inventory of such goods is 10% or less of sales pertaining to such trading activities

Illustration

Use of Range concept

- Range concept can be used for CUP Method as well in addition to CPM, RPM and TNMM. For applying range concept, at least 6 comparable entries in the data set must be available.

- Arrange the data set in the ascending order.

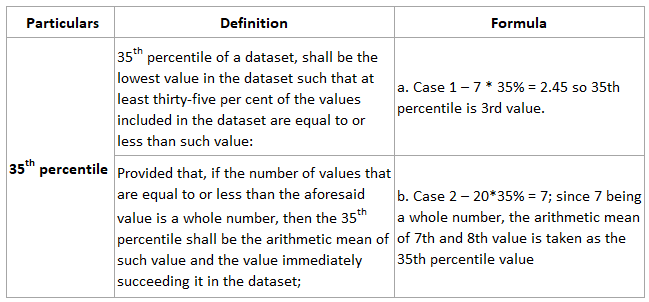

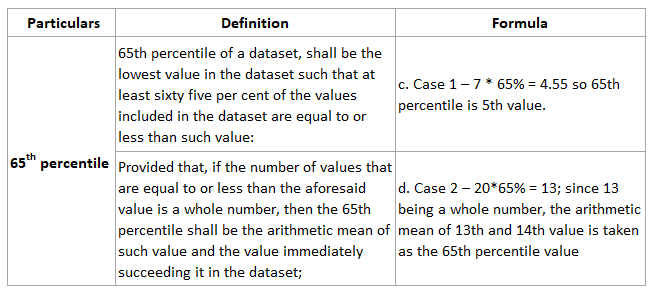

- The arm’s length range would be data points lying between 35th and 65th percentile of the dataset.

- If the transaction price falls within the range, then the same shall be deemed to be ALP. If the 35th & 65th percentile is not a whole number, then value corresponding to the number succeeding the above number should be considered.

- If it is a whole number, then it shall be average of the dataset of such value and the next higher value is to be taken

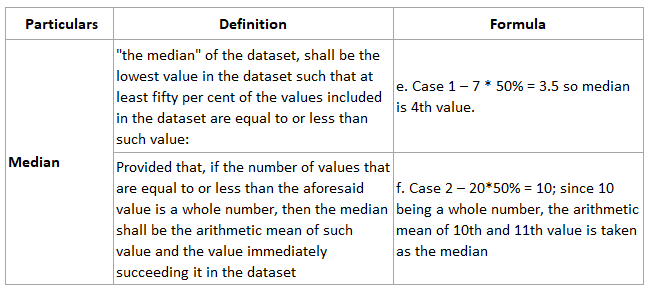

- If the transaction price falls outside the range, the median has to be calculated. Median is the 50th percentile of the dataset. That median is considered as the ALP

Summary of methods and use of range

Reference to percentile

For the purpose of illustration, we shall assume following scenarios:

Case 1 – the dataset has 7 values

Case 2 – the dataset has 20 values

Computation of weights

Question

Where the most appropriate method for determination of ALP of an international transaction is RPM, or CPM or TNMM then, the data to be used for analyzing the comparability of an uncontrolled transaction with an international transaction shall be the data relating to –

- Current year only

- Current year data and financial Year immediately preceding the current year, if the data relating to the Current year is not available at the time of furnishing the return of income

- Data of preceding 3 years

- Data of preceding 2 years

Answer b.

Current year data has to be used. However, financial Year immediately preceding the current year data can be used, if the data relating to the Current year is not available at the time of furnishing the return of income

Question

TTK India Limited enters into certain transactions by way of sale to TTK International (UK) of Rs.24.25 lakhs. It determines arm’s length price of such transaction as Rs.25 lakhs and Rs.23 lakhs under CUP method. Such calculation is made by using two comparable. The arm’s length price of such transaction would be

- Rs. 24.25 lakhs

- Rs. 25 lakhs

- Rs 24 lakhs

Answer a.

Since there are only two comparable transactions, arithmetic mean of the prices has to be computed. The arithmetic mean of Rs 25 lakhs and Rs 23 lakhs is Rs 24 Lakhs. Since the transaction price is excess of ALP, the ALP would be the transaction price, i.e. Rs 24.25 lakhs.

Question

Actual transaction price would be taken as arm’s length price, where variations between the arm’s length price (determined by use of Arithmetic Mean), and actual transaction price does not exceed

- 1% of Arm’s length price – in case of wholesale trading and 3% of Arm’s length price – in case of other business

- 3% of transaction price in all cases

- 1% of arm’s length price

- 1% of actual transaction price – in case of wholesale trading and 3% of actual transaction price – in case of other business

Answer d.

The tolerance band is 1% of actual transaction price – in case of wholesale trading and 3% of actual transaction price – in case of other business

Question

Range concept is applicable when

- More than one price is determined by use of most appropriate method

- Arm’s length price is determined by use of Transaction Net Profit Method (TNMM), or comparable uncontrolled price method (CUP method) or cost plus method (CPM) or resale price method (RPM)

- Six or more comparables are available in the datasets

- All of the above

Answer d.

Range concept is applicable when six or more comparables are available in the dataset, and the most appropriate method is either CUP, CPM, RPM or TNMM.

Question

Range concept is not applicable when

- Most appropriate method is PSM

- Most appropriate method is a combination of two or methods

- Most appropriate method TNMM

Answer a.

Range concept is not applicable for PSM but can be used for CUP, RPM and TNMM

Question

Under Transfer pricing, actual transaction price or profit margin would be accepted if it falls in the range of

- 35th – 65th percentile of the given data set

- 65th – 75th percentile of the given data set

- 25th – 75th percentile of the given data set

- 15th – 35th percentile of the given data set

Answer a.

The range concept prescribes the range to be vale in the dataset between 35th and 65th percentile.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing