Specified Domestic Transactions – Transfer Pricing

Introduction

- The concept of Specified Domestic Transactions (SDT) was introduced in Finance Act 2012. Prior to that the AO were empowered to disallow payments made to related parties which were unreasonable or excessive under section 40A(2)(b) of the Act. Further, TPPs were applicable only for international transactions.

- SC in the case of Re Glaxo Smithkline Asia P Ltd recognised the complications of arriving at the Fair Market value (FMV) in case of transactions involving related parties and suggested why transfer pricing provisions could not be extended to domestic transactions as well

- This led to introduction of section 92BA of the Act and enactment of provisions for Specified Domestic Transactions (‘SDT’).

- Initially the provisions were applicable for transactions covered under 40A(2)(b) of the Act and the threshold limit was INR 5 crores.

- Finance Act, 2015 enhanced the threshold limit from INR 5 crores to INR 20 crores. Finance Act, 2017 amended the section 92BA of the Act by deleting clause (i) – reference to transactions under section 40A(2)(b) thereby further reducing the compliance requirements

- Currently, the provisions are applicable only for transactions involving units enjoying tax holiday benefits [ section 80A, 80-IA(8), 80-IA(10), 10AA], where the aggregate of transactions during the year exceed INR 20 Crores.

Meaning of SDT

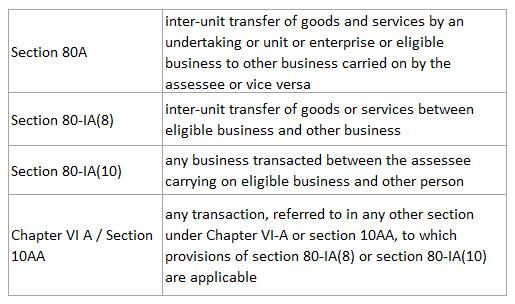

- As per section 92BA, for the purpose of sections 92, 92C (Computation of arm’s length price), 92D (Maintenance and keeping of information and documents) and 92E (Furnishing of report from an accountant), in case of an assessee the specified domestic transaction shall mean any of the following transactions, not being an international transaction, namely

Features of SDT

- Basically, SDT covers transactions which take place between closely held enterprises where one of the enterprise enjoys profit-linked deductions.

- If one unit of an entity enjoys profit-linked deductions (SEZ units) while others don’t (DTA), then provisions of SDT are applicable

- The idea behind such provision is to ensure that the transfer price in such transactions is not fixed in such a way that the entity that enjoys profit-linked deduction does not garner more than its due share of profits from a transaction.

- Once any domestic transaction falls within the ambit of section 92BA, it would be treated in the same way an international transaction is to be treated. Method of determining ALP, documentation to be maintained, reference to TPO, penalty provisions are all similar to international transaction.

- It has to be noted that SDT provisions are applicable only if the aggregate value of such transactions is Rs 20 crores or more during any previous year.

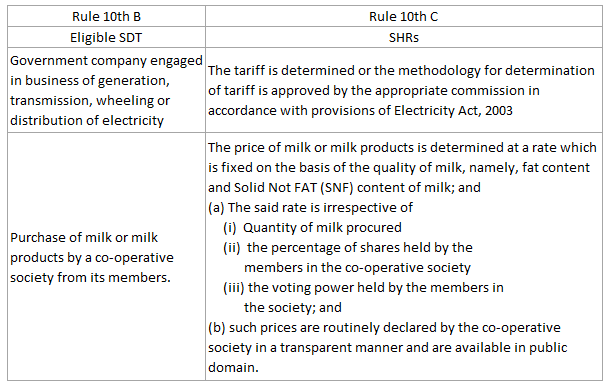

Safe harbour rules for SDT

- Initially, SHRs were provided only for international transactions. However, CBDT extended the SHRs for SDT subsequently.

Question

Xerox Limited is claiming profit linked deduction under section 80-IA and it has obtained certain services amounting to Rs.12 crore with its other Indian group concern during the FY 18-19. In this case Xeros India is

- Not Required to maintain documentation under Rule 10D as it is a specified domestic transaction

- Required to maintain documentation under Rule 10D as aggregate value of transaction is more than 1 crore

- Not Required to maintain documentation under Rule 10D as provisions of specified domestic transaction are not applicable

Answer c.

Once SDT is applicable, the documentation requirement shall be applicable. However, in this case, SDT is not applicable, since the aggregate value of the SDT is only Rs 12 crores, as the threshold limit is Rs 20 crores.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction [Section 92B] – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing

{kind=link}