Introduction to Transfer Pricing

Transfer Price

- “Transfer Price” is the price at which an enterprise charges for its transaction within its group entities

- International transaction involves more than one tax jurisdiction, and due to disparity in tax rates and method of computing income, the parties may try to adjust the transfer prices

- Since the parties are related there is a possibility that the price at which the transactions are carried out can be fixed in such a way that profits can be parked in the country which has less tax and entity in high tax country earns less or no profits

- This would allow the Multinational Enterprise’s to reduce overall tax cost.

- To reduce the tax arbitrage, the principal of Arm’s Length Price (‘ALP’) is applied

- ALP is the price that independent enterprises would charge between them for a particular transaction. Transfer pricing is a process of arriving at the price for goods and services which are transacted between entities which are under a common control under the assumption that they are independent parties

- The transactions may be in the form of purchase, sale, interest, royalty, services, reimbursement etc.

Necessity for Transfer Pricing Provisions

- MNE operate in different countries under various models such as subsidiary, branch, project office, liaison office etc.

- However, true comparison between an independent transaction and related party transaction is often not possible due to many commercial and financial conditions governing a transaction

- Further, in many situations, related parties enter into transactions which normally independent enterprises would not enter into, such as license of intellectual property and so on

Practical difficulties in applying ALP

- True comparison difficult

- It might be impossible to find an uncontrolled comparable transaction which could make the comparison difficult

- Availability of data and reliability of availability data

- Timely availability of data and their reliability would pose a problem in applying TP provisions

- Absence of market price for certain transactions

- Some transaction between related parties may be unique and unrelated parties may not engage in similar activities which makes it difficult to compare.

- Absence of market price including transactions involving “intangibles”

- When the transaction involves intangibles, valuation and pricing is a big problem and may distort the pricing mechanism.

- Administrative burden

- Applying the TP provisions would cause additional administrative burden on the assessee.

- Time lag

- The agreement between the related parties would have been entered in a different time and the transaction at a different point of time and the assessment at a different point of time. The taxpayer may not have relevant information at the time of entering the agreement with related parties. The information regarding market price of similar products or services at would be different at different period of time and time lag would cause difficulties in applying the Arms’ length price.

Question:

Why are Transfer Pricing Provisions needed? Which of the following is an appropriate reason?

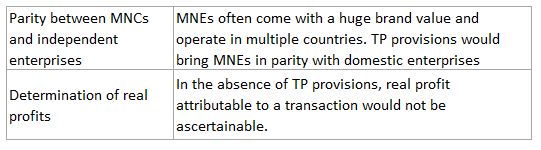

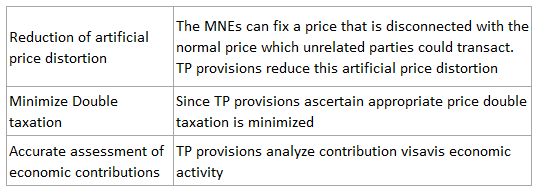

- To bring parity between domestic enterprises and MNEs and to make accurate assessment of economic contributions

- To minimize double taxation

- To reduce artificial pricing distortion and determine real profits

- All of the above

Answer d.

- Transfer Pricing Provisions are required not only to bring parity between domestic enterprises and MNEs but for other reasons such as to minimize double taxation, to reduce artificial pricing distortion and determine real profits.

Transfer Pricing provisions in India prior to 2001

- Transfer pricing provisions existed prior to 2001 by way of section 92 of the Income Tax Act, 1961 (‘Act’) and Rule 10 and Rule 11 of the Income Tax Rules, 1962 (“Rules’)

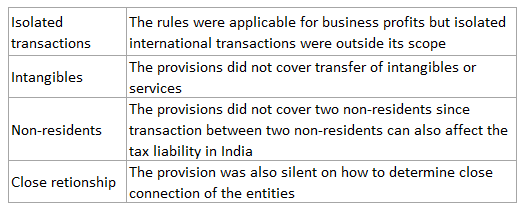

- The provisions required the AO to examine the transactions between closely connected entities (between resident and non-resident) to ensure that reasonable profits are being made from the transactions

- In case of no profit or less than normal profits to the Indian resident, the AO is obliged to apply the rules to arrive at the reasonable profit

- Normal profits would be such % of the turnover, which arises or arrives to the non-resident as the AO may consider reasonable

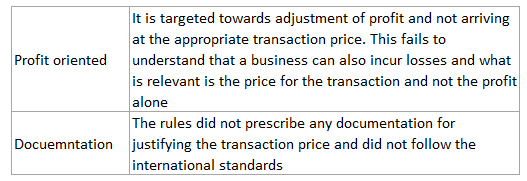

- It is pertinent to determine normal profits as % of sales and there was no prescribed methodology to compute the specific price of any transaction. In other words it was profit specific and not transaction specific.

- The Act however, gave powers to the AO to compute profits in such other manner as he deems suitable

This has many shortcomings:

Transfer Pricing rules and regulations

- Transfer Pricing Regulations (‘TPR’) or Transfer Pricing Provisions (‘TPP’) was included in Chapter X of the Act, through the Finance Act, providing for mechanism to compute income of cross border transactions.

- Older section 92 was substituted with section 92, 92A, 92B, 92C, 92CA, 92D, 92E and 92F.

- This marked a paradigm shift in the way cross border transaction between related entities were assessed.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing