Advance Pricing Agreements (APA)

APA objective

- APA is an agreement between the taxpayer and the taxing authority on an appropriate transfer pricing methodology for a set of transactions over a fixed period of time in future. Section 92CC empowers the Board to enter into APA with any person undertaking an international transaction.

- Purpose of APA: the APA shall relate to an international transaction to be entered into by such person. The APA shall be entered into for the purpose of determination of ALP or specifying the manner in which ALP shall be determined.

- The budget 2020 has extended the scope of APA to include determination of income (Attribution of profit) under section 9(1)(i) of the Act of the PE. Benefit of rollback is also extended to such PEs. This provision would apply to APA which is entered into on or after April 1, 2020

- Any methods referred in 92C(1) with necessary adjustment or variation shall be used to determine the ALP

- Section 92CC shall apply overriding the provisions of section 92C or 92CA.

- The APA shall be valid for such period as specified in the agreement which shall in no case exceed five consecutive years.

- The assessee may choose to enter into APA for specified international transaction instead of all international transaction

- The APA is be binding on the assessee in respect of such international transaction and the tax authorities

- The APA shall not be binding if there is any change in law, or facts bearing such APA

- If the CBDT finds that the APA has been obtained by fraud or misrepresentation of facts, the CBDT is empowered to declare such APA as void ab initio with the approval of the CG.

- Rule 10F to 10T and Rule 44GA deals with various conditions and procedural aspects of the APA.

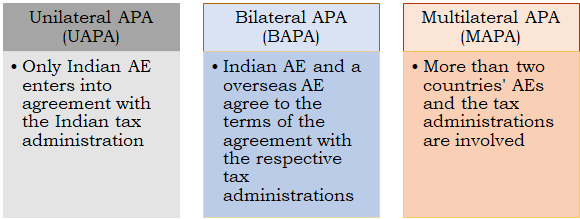

Types of APA

Procedure for filing APA

Eligibility

Any person who undertakes an international transaction or is contemplating to undertake an international transaction shall be eligible to apply for APA with DGIT (International Taxation). Further Budget 2020, has extended the APA to PEs in India for determination of income / attribution of profits.

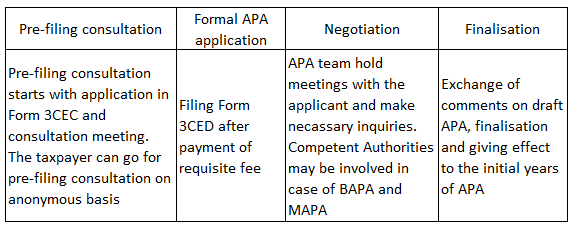

Pre-filing consultation

The APA procedure allows pre-filing consultation on an anonymous basis. The pre-filing consultation is not binding on the assessee. It is generally conducted to determine the scope of the agreement, identify transfer pricing issues and discuss board terms of agreement

Due date of application

Any person who is eligible and desirous can apply to enter into APA can furnish an application form (Form 3CED) along with proof of payment of requisite fee to DGIT(IT) in case of unilateral agreement and to the Competent Authority in India in case of bilateral or multilateral agreement.

The application may be filed at any time before the 1st day of the previous year relevant to the first assessment year for which the application is made. However, if the assessee proposes to undertake international transaction during the year, an application can be made before the entering into such transaction.

Other miscellaneous issues

The applicant may withdraw the application any time before the finalization of the agreement. Defects if any in the application, noticed by the DGIT in case of unilateral agreement or CA in India in case of multilateral agreement shall send a deficiency letter to the applicant to rectify the application within 30 days of receipt of application. The application can also modify the application within 15 days or such other extended period but the number of days cannot exceed 30. The DGIT or the CA as the case maybe can pass an order that the application shall not be proceeded with but not without giving an opportunity to the applicant. The fee would be refunded in such a case

APA finalization process

- The team or the Competent Authority (CA) in India or their representatives shall process the application in consultation with the applicant

- They may hold meetings, call for additional documents, visit the applicant’s premises, make such enquires that deem fit

- The team which make the enquiry will prepare a draft report and forward the same by the DGIT to the CA in India.

- The DGIT (unilateral agreement) and CA (multilateral and bilateral agreements) shall along with the applicant prepare the proposed draft agreement for approval

- The agreement shall be entered by the Board after the approval of the Central Government.

- Once the agreement is signed, a copy of the agreement would be sent to the jurisdictional commissioner

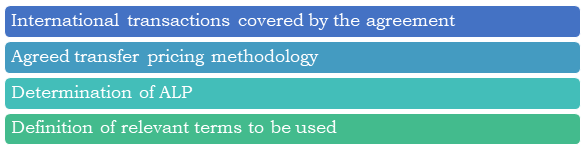

Terms of the agreement

- The agreement may include the following:

Impact of the agreement

- The agreement is binding on the assessee and the tax authorities with regard to the specified international transactions

- The agreement shall not be binding on the Board or assessee if there is any change in critical assumptions or failure to meet conditions specified in the agreement

- The binding effect of agreement shall cease only if any party has given due notice of the concerned other party or parties.

- If there is a change in any critical assumptions or failure to meet the conditions, the agreement can be cancelled or revised as the case may be.

APA process summary

Rollback provisions

- In order to reduce current pending as well as future litigation in respect of the transfer pricing matters, section 92CC(9A) provides rollback mechanism in the APA scheme.

- Accordingly, the APA may, provide for determining the ALP or for specifying the manner in which ALP is to be determined in relation to an international transaction entered into by a person during any period not exceeding four years preceding the first of the previous years for which the APA applies.

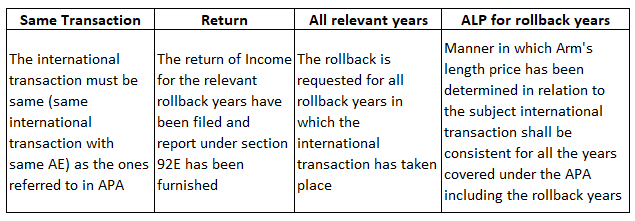

- Rollback option is not available to an applicant in the following circumstances.

Circumstances when rollback option can be applied

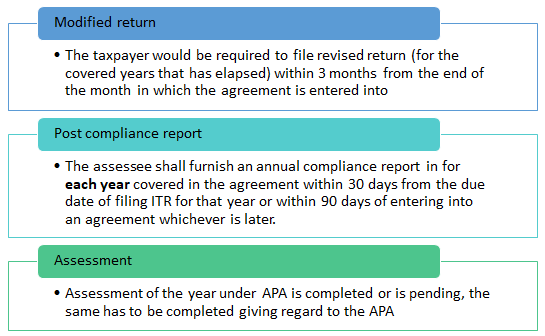

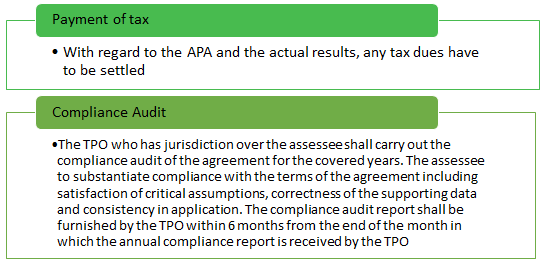

Post compliances of APA

Question

Multilateral advance pricing agreement is an agreement between

- Assessee and CBDT

- Assessee, its AEs and CBDT

- Assessee, two or more foreign tax authorities, two or more AEs

Answer c.

A multilateral APA is between assessee, two or more foreign tax authorities, two or more AEs

Question

Zoxo India enters into an APA for determination of ALP of Technical services availed from Zoxo Inc (USA). Such advance pricing agreement shall be binding on

- Zoxo India only

- Zoxo India and the AO

- Zoxo USA and Zoxo India

Answer b.

The APA is binding on Zoxo India and the jurisdictional AO.

Question

Quark India proposes to enter into technical service agreement with its group company with effect from 1st August 2020. When is the last date for filing application for APA?

- March 31, 2020

- March 31, 2021

- July 31, 2020

Answer c.

If the transaction is not an existing international transaction but a new transaction, then APA has to be applied before commencing the transaction i.e. Application on or before July 31, 2020

Question

Indian company enters into an advance pricing agreement for the PY 2018-19 for international transaction with foreign associated enterprise which it has undertaken from PY 2011-12. In this case the rollback year means

- 2018-19, 2017-18, 2016-17, 2015-16

- 2017-18, 2016-17, 2015-16

- 2017-18, 2016-17, 2015-16, 2014-15

Answer c.

The applicant has to either apply for all the four years or not apply at all. However, if the covered international transaction did not exist in a rollback year or there is some disqualification in a rollback year, then the applicant can apply for rollback for less than four years

Question

The benefit of rollback would not be available for preceding four years under advance pricing agreement when:

- Return for one of the four years is filed u/s 139(4) – belated return

- No return of income has been filed u/s 139(1) for one of the roll back years

- Accountant’s report has not been filed for one of the rollback years

- All of the above

Answer d.

Rollback benefit is not available if the return for the rollback years are not filed within the due date. Also, if there is failure on the assessee to file Accountant Report for the rollback years then rollback benefit is not available.

Question

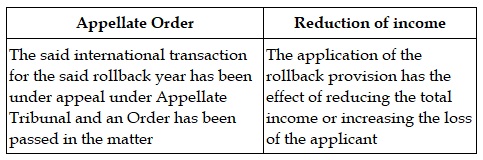

Roll back provision shall not be provided in respect of an International transaction for a rollback year if

- Appellate tribunal has passed an order on determination of ALP of the said International transaction for the said year at any time before signing of the agreement

- The application of rollback provision has the effect of reducing the total income or increasing the loss, as the case maybe, of the applicant as declared in the return of income in the said year

- Such international transaction is different from International transaction for which advance pricing agreement is made

- All of the above

Answer d.

Roll back provisions would not be available if ITAT has passed an order on determination of ALP of the said International transaction for the said year at any time before signing of the agreement, or the application of rollback provision has the effect of reducing the total income or increasing the loss, as the case maybe, of the applicant as declared in the return of income in the said year or such international transaction is different from International transaction for which advance pricing agreement is made

Question

A Ltd has entered into an APA on the following transaction for AY 2019-20 and next consecutive 4 years. The covered transaction is software services to its AE in USA. During the AY 2021-22, the assessee proposes to undertake similar transaction (identical terms) with another AE in UK. Can the APA agreement be applicable to this transaction?

- APA agreement is transaction specific. Since the terms are identical, the same agreement can cover the transaction with UK AE as well.

- APA agreement is both transaction and AE specific.

Answer b. APA agreement is both transaction and AE specific. Though the terms are identical, the agreement cannot be extended to include a different AE. At best the APA can be held to be persuasive value for the UK AE transaction.

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Dispute Mitigation strategies in transfer pricing

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing