Dispute Mitigation strategies in transfer pricing

- Determining ALP is not an exact science and often may lead to different answer depending on many factors.

- This has resulted in huge litigation leaving the assessee and the income tax authorities often in the loggerheads.

- The data available at the time of concluding the agreement / work order, the data at the time of preparing documentation and filing return of income, and the data available at the time when the issue is taken up during the assessment would be widely varying.

- This has resulted in disputes running into crores and uncertainty in the minds of overseas investors.

- The traditional way of handling dispute is going through the grind of appeal process which takes years to complete and with a huge cost.

- The Government has thought about this conundrum and has come out with various mechanism which can be taken up by the assessee to bring in certainty or to reduce litigation. Each initiative has its own share of advantages and disadvantages.

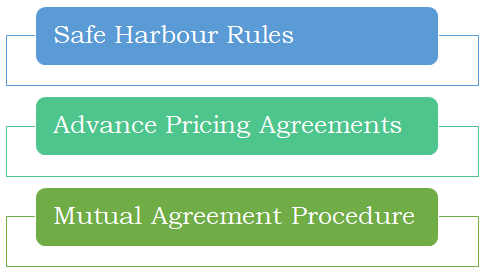

- Following are the mitigation strategies

- Advance ruling is also available for non-residents for determining the taxability of a transaction.

- However, advance ruling would not apply for the cases which involves determination of fair market value.

- Since determination of ALP is akin to determination of Fair Market Value, transfer pricing transactions cannot be subjected to Advance Ruling.

Safe Harbour Rules

- In order to reduce the litigation and in alignment with the best international practices, Safe Harbour Rules (‘SHRs’) were introduced.

- Section 92CB and Rules 10TA to 10TG provide the framework for SHRs.

- ‘Safe Harbour’ has been defined to mean circumstances in which the Income Tax Authorities shall accept the Transfer Price declared by the assessee.

- SHRs were introduced to primarily determine ALP. However, budget 2020 has extended the application of SHRs for determination of income (attribution of profits) under section 9(1)(i) of the Act to a PE. This would be applicable for AY 2020-21 onwards.

Features of SHR

- It is an alternate dispute resolution mechanism where the assesse declares a margin specified in the rules and the department accepting the price which significantly reduces the scope of litigation and money being locked up in demand.

- SHR was initially introduced in the year 2013 applicable for 5 years beginning from FY 2012-13 to FY 2016-17

- On 7th June 2017, the CBDT issued a notification amending the SHRs by extending the applicability to an additional category of international transaction as well as revising the applicable price/margins that would be accepted as arm’s length.

- The safe harbor provisions are now extended up to FY 2018-19 with certain modifications in thresholds for the eligible international transactions. The safe harbour rules are due for renewal for FY 2019-20 and future years.

- For FY 2016-17, the taxpayer has the option to opt for the safe harbors under the old rules or the amended rules, whichever is more beneficial.

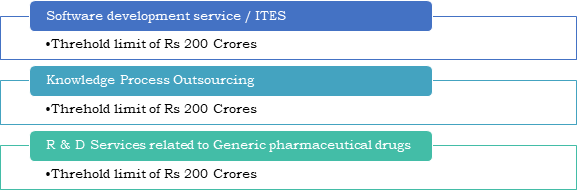

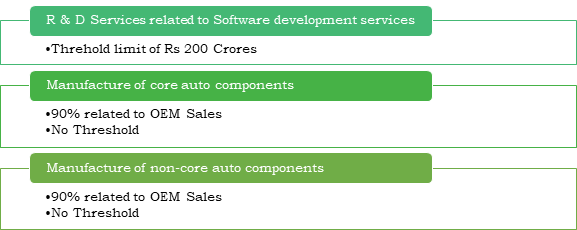

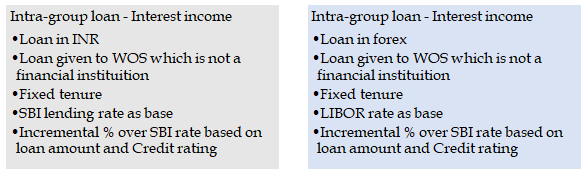

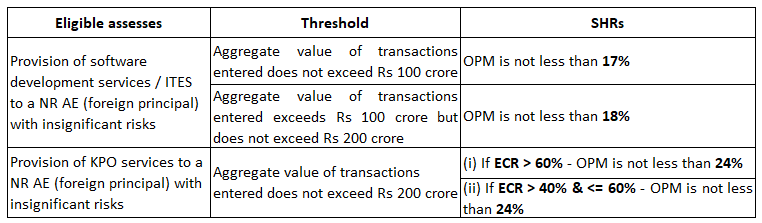

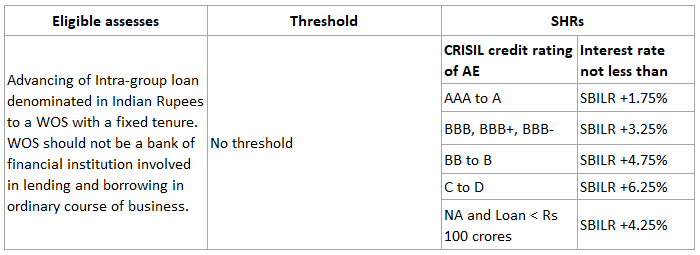

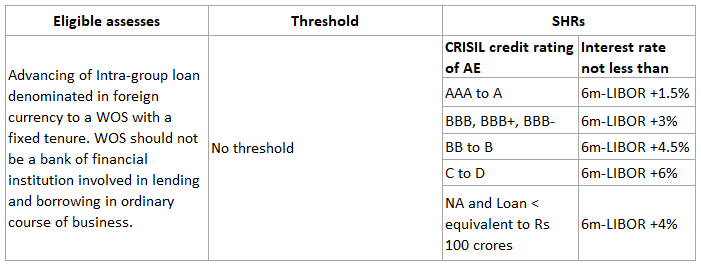

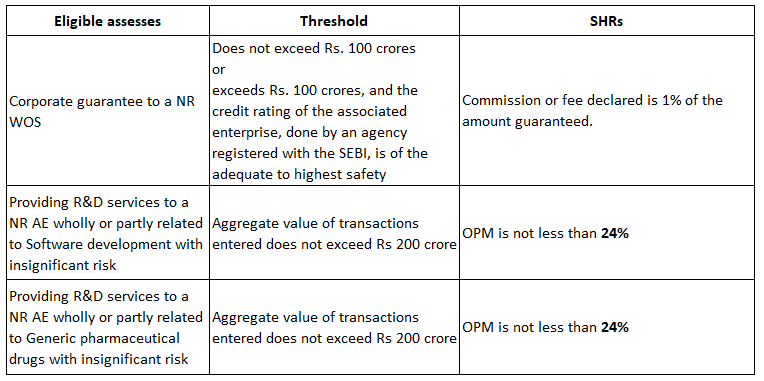

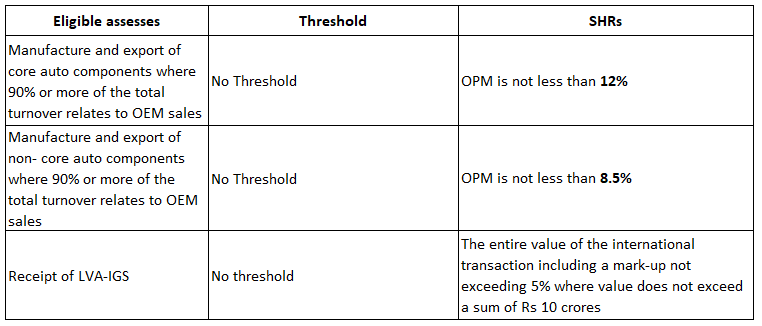

Eligible services for SHR

- Export / Services provided by a person resident in India or a non-resident having a Permanent Establishment in India to a non-resident Associated Enterprise. The margins are provided

Eligible services for SHR

Some Safe harbour rules

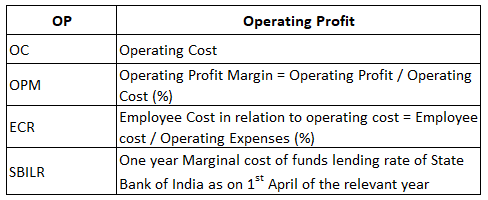

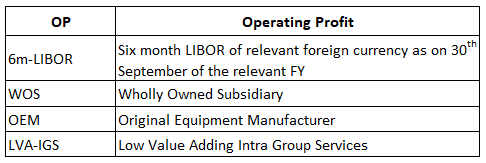

- Certain abbreviations used in the table indicating safe harbour provisions

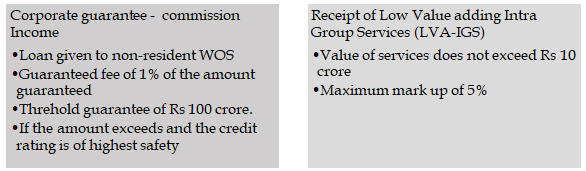

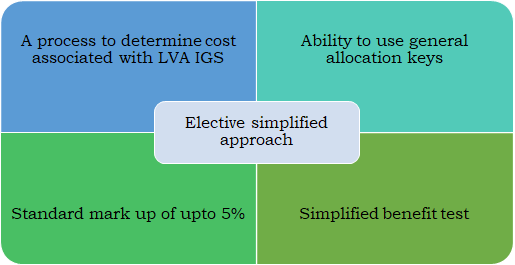

Low Value Adding Intra Group Services

- Payment towards intra-group services has been a great deal of controversy between the MNE group companies and the tax authorities.

- Intra group services possess a unique problem that other transaction may not have.

- Generally, many MNEs would setup back office centers across the globe to provide support and or ancillary services to group companies.

- This may range from routine book keeping, accounting, HR services to complicated services such as treasury, investment decision making etc.

- The uniqueness stems from the fact that normally such services are not taken from unrelated entities or there is no active market for certain services to benchmark the transactions.

- Often these entities are compensated on cost plus basis.

- The difficulty arises to benchmark what would be the appropriate margins over the cost.

- In most cases, the service provider would not be assuming any significant risk.

- In the process to align transfer pricing outcomes with the value creation, OECD lays down extensive guidance on dealing with matters of LVA IGS

- LVA IGS are performed by one or members of an MNE group on behalf of one or more other group members. LVA IGS are

- Supportive in nature

- Are not part of the core business of the MNE group

- Do not require use of unique or valuable intangibles and do not lead to creation of one

- Do not involve assumption of significant risk by the service provider

- The guideline prescribes a mark-up of 5% for the qualifying activities

Question

What would be the operating margin under safe harbor rules where value of KPO services with insignificant risk is Rs.300 crores?

- 24% or more where employee cost to operating expense ratio is 60% or more

- 21% or more where employee cost to operating expense ratio is 40%-60%

- 18% or more where employee cost to operating expense ratio is 40% or less

- None of the above

Answer d.

The safe harbor rules are not applicable for KPO services where turnover exceeding Rs 200 crores

Question

What would be the mark-up on cost under safe harbor rules where value low value adding intra-group services is Rs.5crores?

- 5% or less

- 5% or more

- 8.5%

- 10%

Answer a.

Under SHRs, LVA-IGS for payment not exceeding Rs 10 crores, the mark-up on cost can be 5% or less

Income from transaction with Non-Residents – Transfer Pricing

Transfer pricing adjustment and consequence

Advance Pricing Agreements (APA)

Fundamentals of Base Erosion and Profit Shifting – Transfer Pricing

Anti-Avoidance measures in certain jurisdictions – Transfer pricing

Returns, Audit and other miscellaneous provisions – Transfer pricing

Determination of ALP – Transfer Pricing

Arm’s Length Principle – Transfer Pricing

Specified Domestic Transactions – Transfer Pricing

Secondary Adjustment – transfer pricing

International Transaction [Section 92B] – Transfer Pricing

Additional reporting by Multinational companies – Transfer pricing

Economic analysis – Transfer Pricing

Limitation of interest deductions – transfer pricing

Penalties for non-compliance – Transfer Pricing

{kind=link}